Disclaimer.

This article reflects publicly reported data and analysis as of March 25, 2026. Fuel reserves, prices, and supply chains are dynamic, verify latest figures via government sources (DCCEEW, ACCC) and industry updates.

Projections on outcomes (e.g., crop yields, rationing) are based on current trends and historical patterns; actual events may differ.

Opinions, thoughts, ideas and views expressed are those of the author only.

Article Summary.

Australia’s fuel and urea supplies are critically strained by the Strait of Hormuz closure to Western shipping, which disrupts Asian refineries supplying over 80% of imported diesel and two-thirds of the 95% imported urea.

Diesel demand has surged 25-50% amid over 550 dry stations and rationing queues, powering essential sectors like freight and mining, while urea shortages risk 2026-27 crop yields and AdBlue-induced truck shutdowns.

Government measures provide short-term relief but fail to address structural vulnerabilities, urging strategic reserves and diversification.

Top 5 Takeaways.

1. Australia is facing two linked supply crises: Diesel and urea are tightening at the same time and both pressures originate from the Strait of Hormuz. As the article notes, “fuel and urea are not independent crises… they are structurally linked.”

2. Diesel shortages threaten the core functions of the economy: Freight, agriculture, mining, waste collection and emergency services all depend on diesel. Demand has surged to between 125 and 150 percent of normal levels and more than 550 stations have already run dry on at least one fuel type.

3. Urea supply is collapsing at the worst possible moment: Australia imports over 95 percent of its urea and two thirds normally move through Hormuz. Current stocks “are expected to be exhausted by mid April” which directly threatens the winter cropping window and 2026–27 yields.

4. AdBlue introduces a mechanical stop to the freight fleet: Modern diesel engines derate and then refuse to start without AdBlue. As the article states, “their vehicle stops, and it does not restart until AdBlue is sourced and filled.” This is not a gradual slowdown. It is a hard limit.

5. Government measures help: However, they do not resolve the structural exposure.

Table Of Contents.

1.0 What’s Happening In Australia with Fuel and Urea?

2.0 How Australia’s Fuel Supply Actually Works.

3.0 Why Diesel Is the Dominant Concern.

4.0 What the Government Has Done and What It Has Not Said.

5.0 Urea: The Second Crisis Running in Parallel.

6.0 The Yara Pilbara Factor.

7.0 AdBlue and the Mechanical Hard Stop in Australia’s Freight Fleet.

8.0 The Reinforcing Loop Between Fuel and Urea.

9.0 A Comparison of Current and Projected Positions.

10.0 What the Policy Response Should Include.

11.0 The Indicators Worth Watching.

12.0 What the Current Position Means for Australia.

13.0 Conclusion.

14.0 Verify the Facts Yourself.

1.0 What’s Happening In Australia with Fuel and Urea?

We’ve arrived at a moment that decades of energy policy reviews warned was possible. Two essential industrial chemicals, diesel fuel and urea, are simultaneously under supply pressure from the same geographic source.

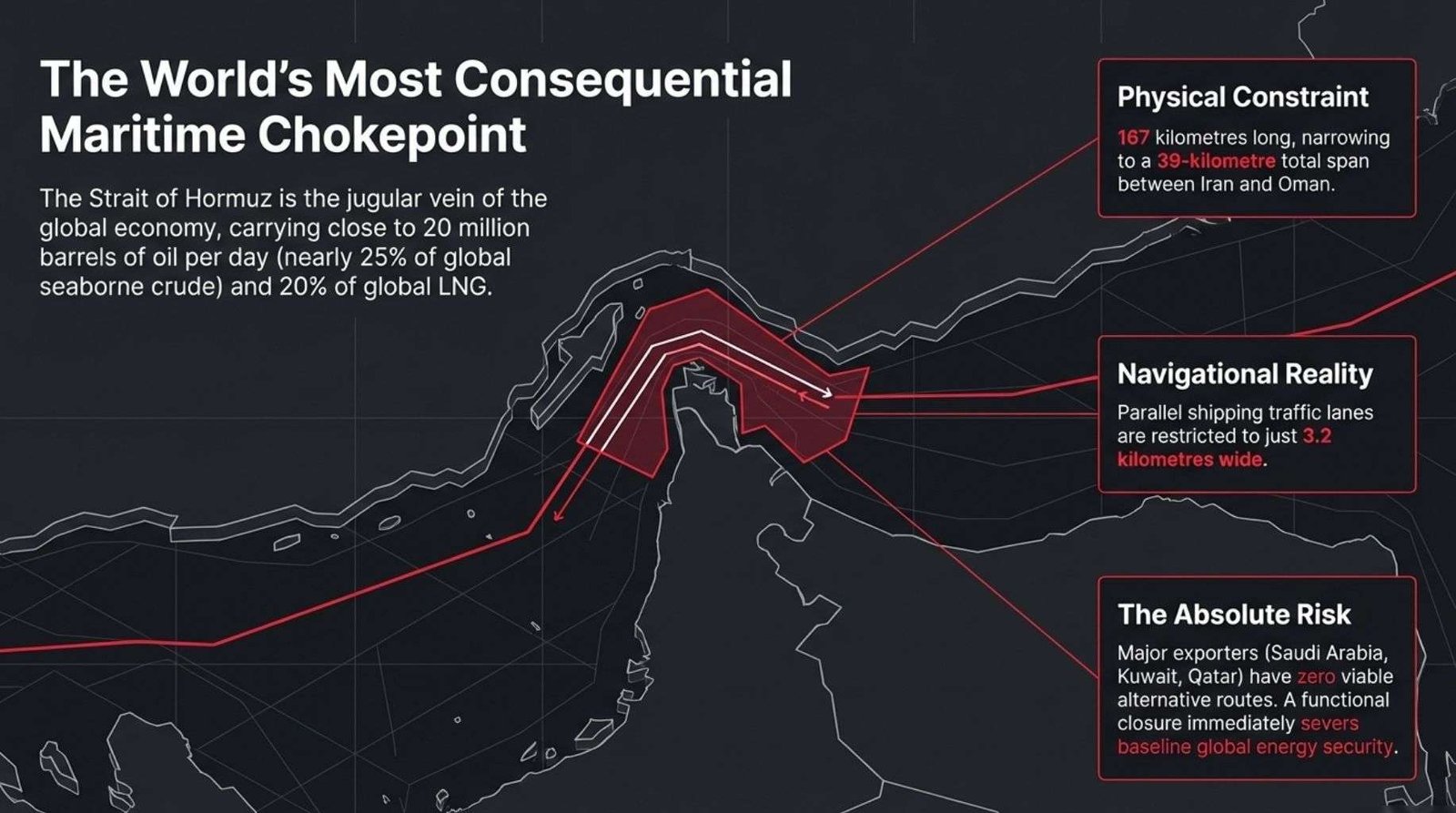

The Strait of Hormuz is the world’s most important maritime chokepoint.

It’s the only sea passage that links the Persian Gulf to the open ocean and it has become the single most consequential piece of water for Australian supply chains right now.

The strait runs for about 167 kilometres in length and narrows to 39 kilometres between Iran and the Musandam Peninsula of Oman.

The strategic pressure comes from the level of traffic that must pass through a very confined space.

All international shipping is directed through a formal Traffic Separation Scheme that uses two parallel lanes.

Each lane is only 3.2 kilometres wide and the two lanes are divided by a buffer zone of the same width.

Even with these tight dimensions the strait carries close to 20 million barrels of oil each day which is almost a quarter of global seaborne crude.

It also carries about 20 percent of the world’s liquefied natural gas.

Its vulnerability is unmatched because major exporters such as Saudi Arabia Kuwait and Qatar have few workable alternatives.

Any disruption including the regional tensions seen in early 2026 creates an immediate risk to global energy security.

It pushes up insurance costs and unsettles supply chains. In practical terms the Strait of Hormuz functions as the jugular vein of the global economy.

Localised friction in this narrow corridor can produce consequences that spread across industries worldwide.

This article does not set out to alarm, not at all, my intent is to explain, clearly and completely, what is happening, why it is happening, what the government is doing about it, and what the next several months are likely to look like for Australian industry, agriculture and the general voting public.

Understanding the situation requires patience with complexity.

Fuel and urea are not independent crises that happen to be occurring at the same time. They are structurally linked and the failure of one accelerates pressure on the other.

The reinforcing nature of the two supply disruptions is the detail that most casual news coverage has not being capturing well enough in my opinion, we deserve a full account of both.

The 27 million+ people who live in this island nation, from those managing freight businesses and farming properties to those simply filling a car at the local servo, need sufficient factual information to make their own assessments about what the situation means for them.

I’m trying to shine a bit of extra light on the situation, set against an honest account of what is known, what is uncertain, and what the realistic range of outcomes looks like from the vantage point of late March 2026.

2.0 How Australia’s Fuel Supply Actually Works.

To understand the current shortage, it helps to understand how Australia has been supplied under normal conditions.

Australia does not produce meaningful quantities of crude oil.

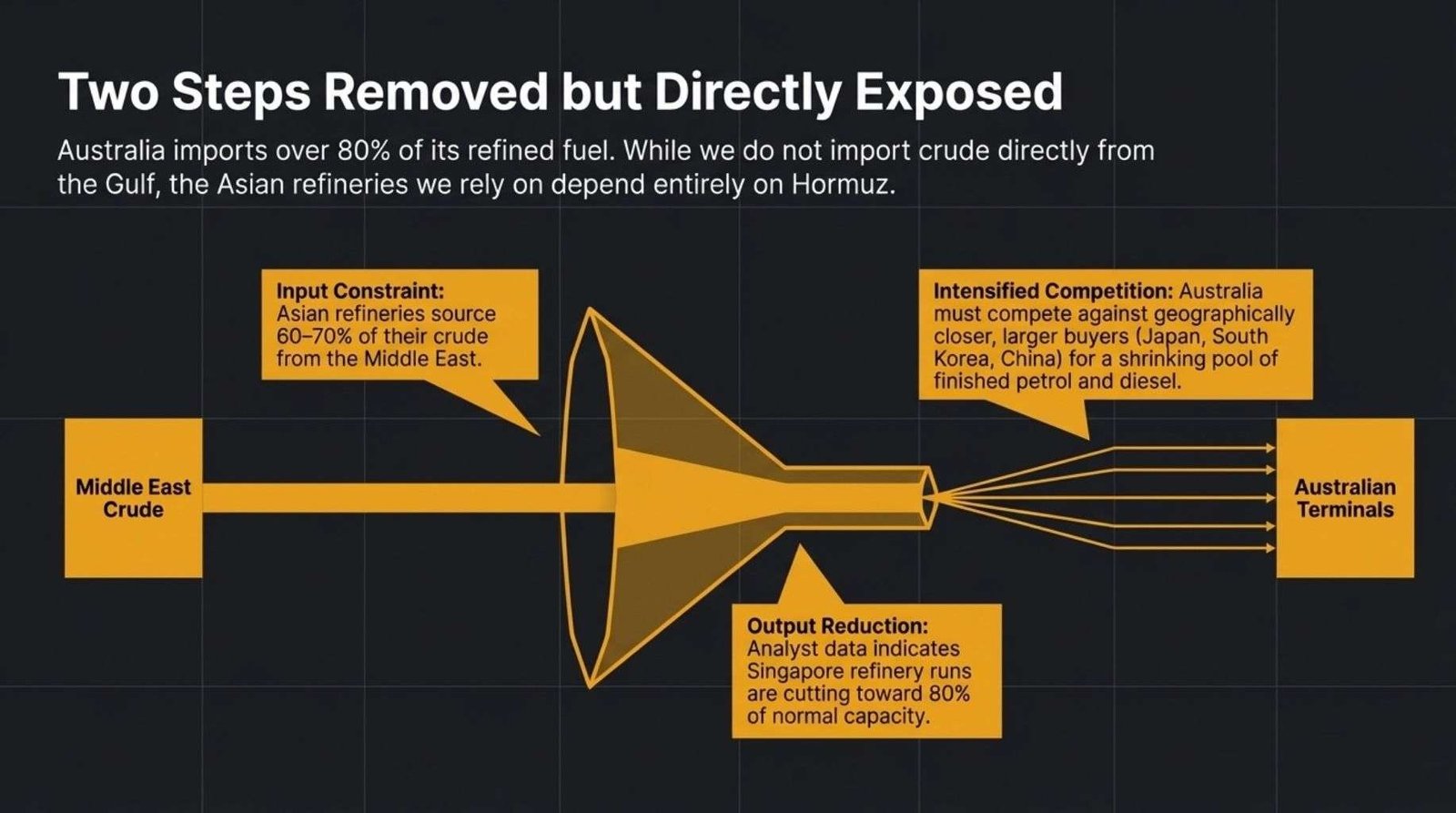

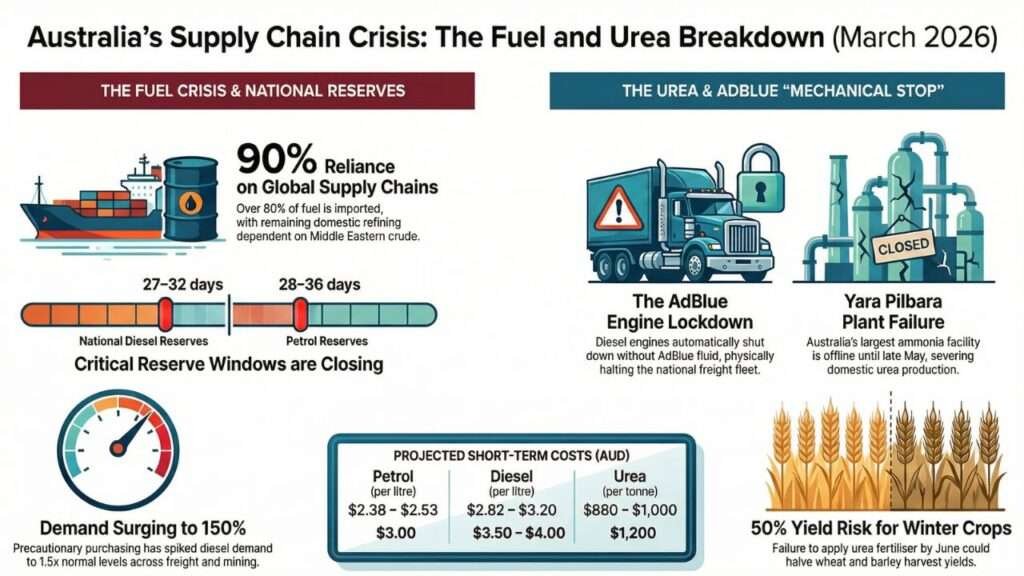

I’m sure by now every person and their dog are fully aware they we import over 80 percent of our refined fuel, with only two operational domestic refineries supplying the remainder, Ampol’s Lytton plant in Brisbane and Viva Energy’s Geelong refinery, together cover well under 20 percent of national demand.

Everything else arrives by ship.

The shipping routes for refined fuel pass through Southeast Asia. Singapore, South Korea and Taiwan are the primary refining hubs that process crude oil into the petrol, diesel and jet fuel that Australian terminals receive.

Here is the critical detail most people miss: those Asian refineries source roughly 60 to 70 percent of their crude from the Middle East, which means they depend on the Strait of Hormuz even when Australia does not receive direct Gulf shipments.

When the Strait closes to Western-aligned shipping, Australia does not just lose a few tanker routes. It loses access to the refineries that turn crude into the fuels it actually imports.

Australia is, in this sense, two steps removed from the primary disruption but still directly exposed to its consequences.

The Singapore connection deserves specific attention, their refining complexes process some of the largest volumes of fuel destined for the Asia-Pacific region.

When Singapore refiners cannot source sufficient Middle Eastern crude, they cut production runs as you would expect.

Lower output from Singapore means fewer barrels of finished product available globally and Australia then competes for that shrinking pool against Japan, South Korea, China and other economies that are geographically closer to the refineries and represent larger long-term commercial relationships.

We are not a trivial customer, but we are not the dominant one either.

Analysts with access to refinery scheduling data have noted that Asian refinery runs may already be cutting toward 80 percent of normal capacity, which implies competition for available barrels will intensify further in the coming weeks.

This competitive dynamic has not received the public attention it warrants.

Following strikes on Iranian infrastructure in late February 2026, the Strait has been functionally closed to Western-aligned tankers.

Energy Minister Chris Bowen has confirmed publicly that at least 6 April fuel shipments have been turned back or deferred.

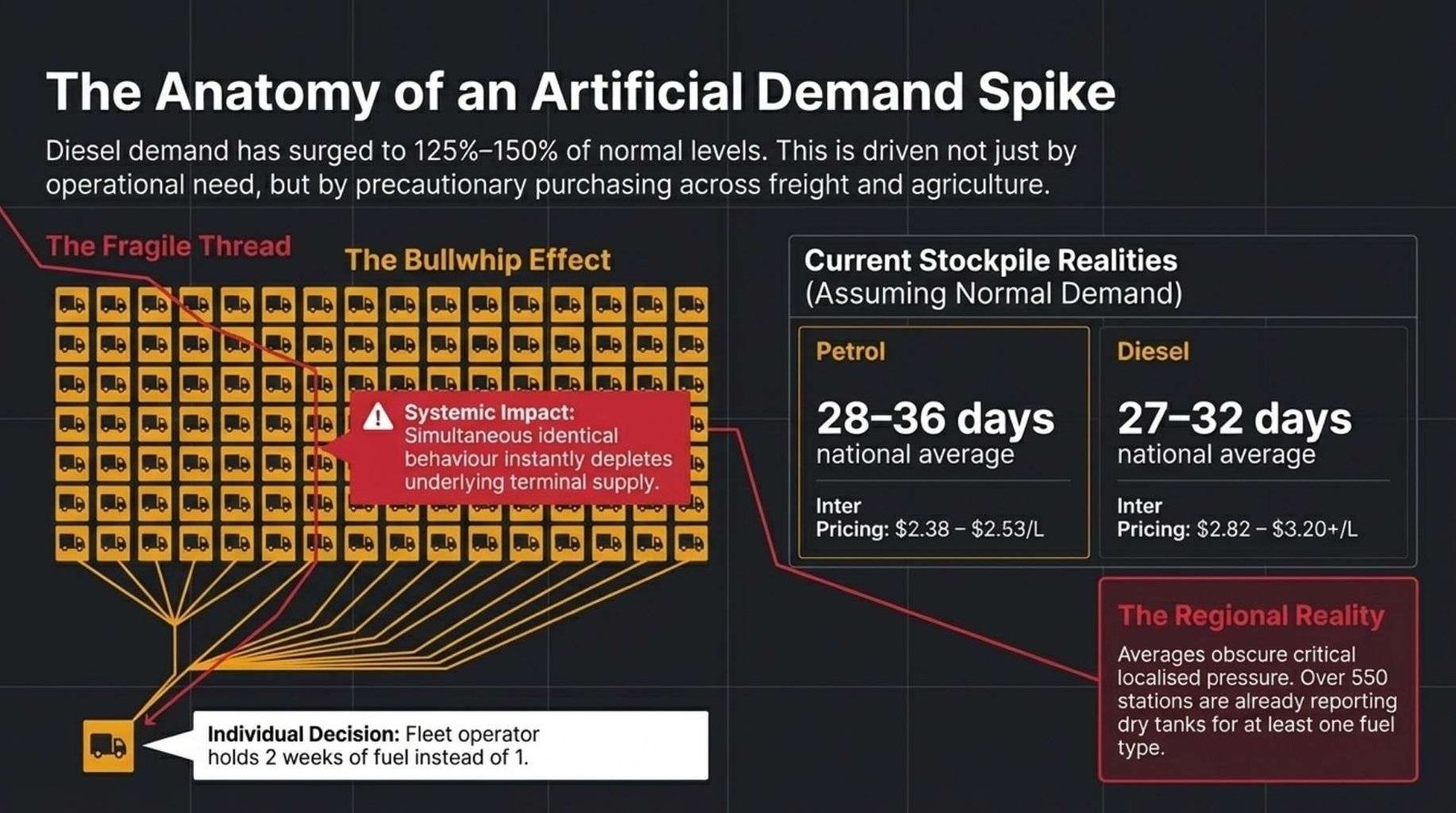

Emergency reserves have been released. Stock cover, assuming normal demand patterns and excluding regional distribution gaps, sits at approximately 28 to 36 days for petrol, 27 to 32 days for diesel, and 29 to 31 days for jet fuel.

Those figures are national averages. Regional figures, particularly in Queensland and New South Wales, are materially worse, and any figure that assumes normal demand is immediately suspect given that demand has already changed substantially.

Over 550 petrol stations across the country are currently reporting they are out of at least one fuel type. Some have introduced self-imposed purchase limits.

The northern Brisbane suburb of Strathpine saw a 90-minute queue at a diesel bowser on the morning of 22 March. That is not illustrative language.

It is what fuel rationing looks like before it is officially called rationing.

3.0 Why Diesel Is the Dominant Concern.

Petrol shortages affect private motorists. Diesel shortages affect the entire economic infrastructure of the country. The distinction matters enormously.

Diesel powers the freight network that moves goods from ports to distribution centres and from distribution centres to supermarkets.

It powers agricultural machinery during planting and harvest. It powers mining operations across the Pilbara, the Hunter Valley and the goldfields of Western Australia. It powers waste collection vehicles, emergency services, backup generators in hospitals, and the refrigerated trucks that keep food cold in transit.

These are not optional or marginal uses. They are the operating requirements of a functioning economy.

Demand for diesel has surged to between 125% and 150% of normal levels since the crisis began, driven partly by genuine operational need and partly by precautionary purchasing across the freight and agriculture sectors.

The precautionary element is worth understanding separately. When a business that runs ten diesel-powered vehicles decides to hold two weeks of additional fuel on-site rather than one week, its individual decision is rational.

When every similar business in the country makes the same decision simultaneously, the collective effect is an artificial demand spike that depletes available supply faster than underlying operational requirements alone would produce.

This is the dynamic that turns a manageable supply reduction into a visible shortage, and it is the dynamic the government’s behavioural messaging is trying to interrupt.

Waste management companies have already flagged publicly that bin collection services may be reduced or paused in some areas if diesel supply cannot be secured at viable prices.

That signal matters because waste collection is a service most Australians regard as background infrastructure, something that simply happens.

When it stops being reliable, the supply disruption has moved from an industrial issue to a residential one.

Fuel prices reflect the supply tightening. Petrol is currently sitting between $2.38 and $2.53 per litre across most capital cities, with isolated stations already charging above $3.00 per litre.

Diesel ranges from $2.82 to above $3.20 per litre, with some regional operators reporting figures above $3.50.

Brent crude has returned to above US$104 per barrel. Analysts modelling a continued Hormuz closure and a 20 percent or greater reduction in Asian refinery output are projecting diesel at $3.50 to $4.00 per litre within weeks.

The ACCC has received over 500 price gouging complaints and new legislation authorises fines of up to $100 million for verified gouging conduct.

The regional dimension is particularly significant. Fuel shortages do not distribute evenly across a continent the size of Australia.

A station running dry in inner Melbourne has different consequences from a station running dry at a roadhouse serving a 400-kilometre stretch of highway in Western Australia’s Murchison region.

The national average obscures significant localised pressure that has real consequences for people in areas with no alternative supply source within reasonable range.

Regional Australians, both communities and industries, are absorbing disproportionate impact from a supply tightening whose causes originate in a conflict 10,000 kilometres away.

That asymmetry is not new to regional Australia, what’s new is its scale.

4.0 What the Government Has Done and What It Has Not Said.

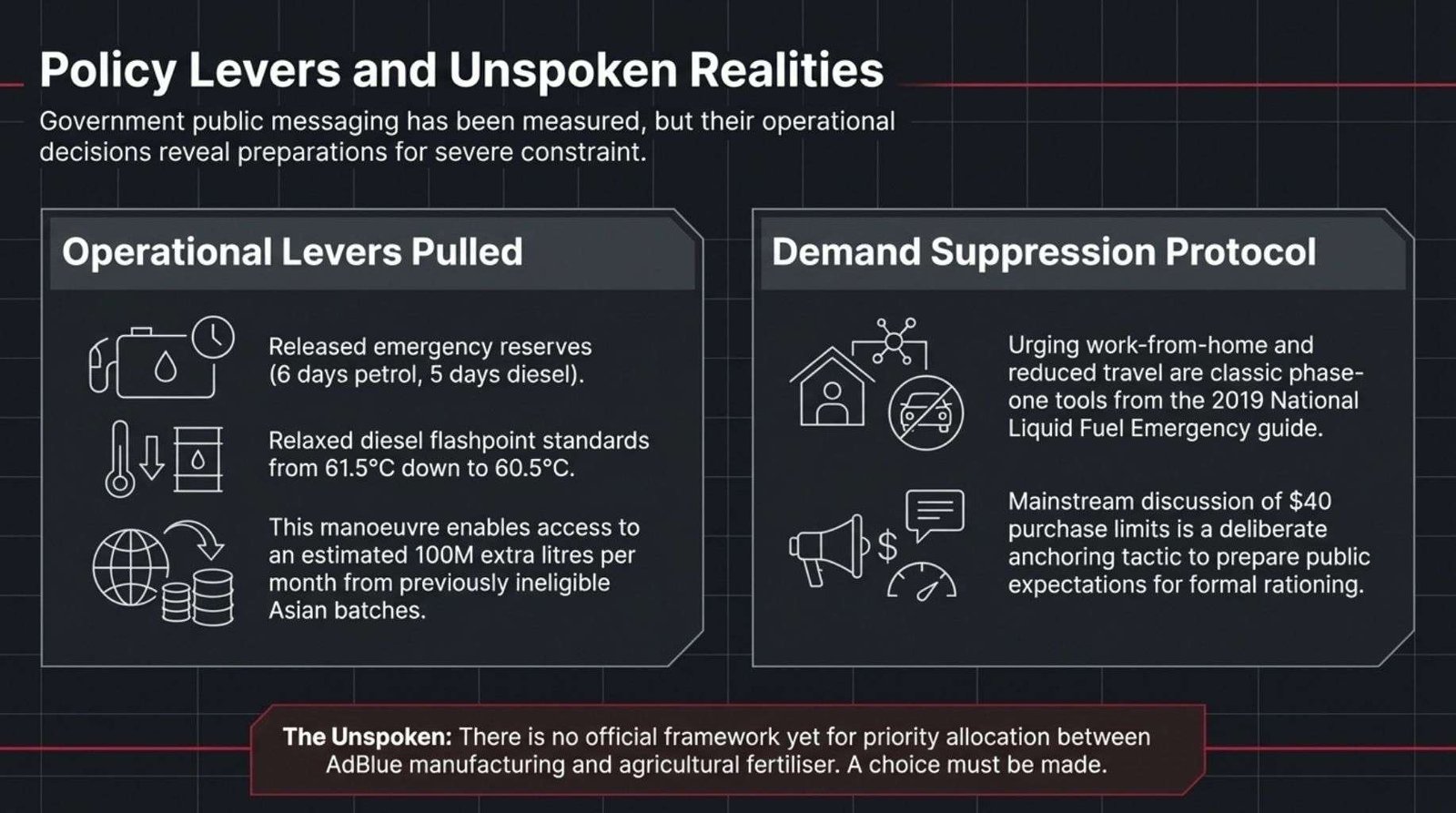

The federal government’s response has been measured in its public language and more revealing in its operational decisions.

Emergency reserves equivalent to approximately six days of petrol and five days of diesel have been released.

Fuel quality standards have been temporarily lowered for a 60-day period, allowing imports of higher sulphur fuel that would normally be off-specification for the Australian market.

The diesel flashpoint requirement has also been relaxed, from 61.5 degrees Celsius to 60.5 degrees, specifically to allow access to a wider range of Asian refinery batches that were previously ineligible.

Together these measures are estimated to add approximately 100 million litres per month to available supply.

The flashpoint change in particular is a clever move because it expands the eligible batch specification without requiring new supplier relationships.

It is also a measure whose operational benefit is real but limited: it draws on a slightly wider pool of the same regional supply base that is already under constraint from upstream crude availability.

The government has urged Australians to work from home where possible, to avoid non-essential travel, to use public transport and to buy only what they need.

These are not suggestions made for environmental or public health reasons. They are the classic demand suppression toolkit deployed in the phase immediately before formal rationing is introduced.

Anyone familiar with how supply-constrained economies have managed fuel shortages historically will recognise the sequence precisely.

The 2019 National Liquid Fuel Emergency Operational Guide, which is a publicly available document, includes a $40 per transaction purchase limit, priority sector fuel allocation lists, a provision to halve business fuel supply allocations, and price-based demand management tools.

The fact that the $40 limit is now a subject of active public discussion in mainstream media is not coincidental. It represents a deliberate preparation of public expectations for measures that may follow.

Governments in this position do not discuss specific rationing mechanisms in public without purpose.

What the government has not said publicly is also informative. There has been no official acknowledgment that priority sector collapse is a near-term risk, despite waste, freight and agriculture sectors all signalling exactly that through their own public statements.

There has been no formal declaration under the Liquid Fuel Emergency Act. There has been no published threshold at which formal rationing would be triggered. And there has been no public commitment to a timeline for when the situation might improve or under what conditions.

The government’s approach is understandable as a communication strategy. Announcing formal rationing before it is operationally necessary risks panic purchasing that accelerates the very shortage it is meant to manage.

The challenge is that soft messaging directed at a public already watching queues at fuel stations and reading about $4.00-per-litre projections may not be sufficient to suppress demand without more explicit guidance on what comes next.

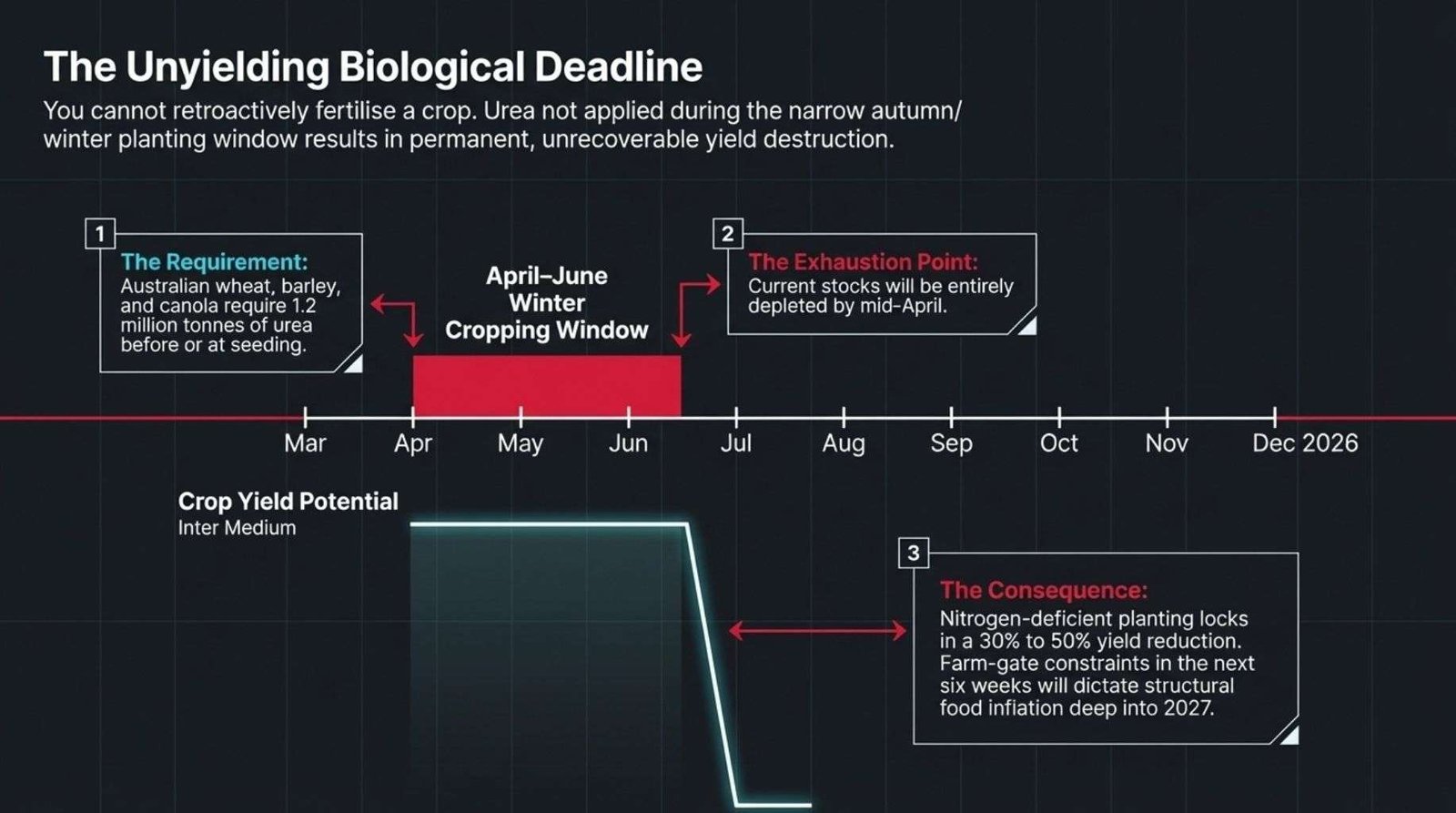

5.0 Urea: The Second Crisis Running in Parallel.

Urea is a nitrogen compound with two primary uses in Australia. It is applied to agricultural land as fertiliser, supplying the nitrogen that grain crops require to reach viable yields.

And it is the active ingredient in AdBlue, the fluid that modern diesel engines require to operate within legal emissions standards.

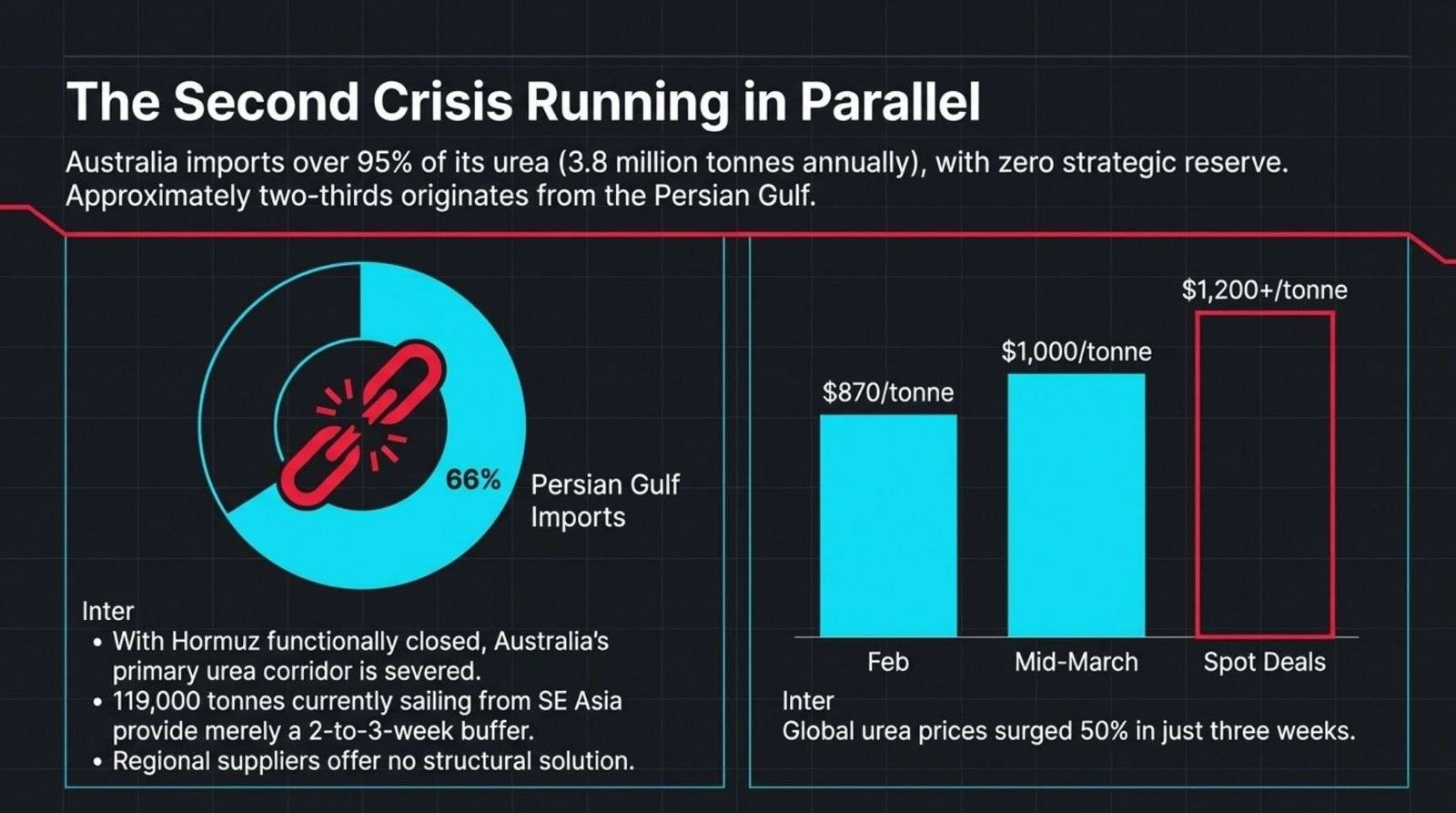

Australia imports over 95 percent of its urea, approximately 3.8 million tonnes annually. Domestic production is negligible. There is no strategic reserve.

Roughly two thirds of those imports originate in the Persian Gulf, from Saudi Arabia, the UAE, Qatar and Oman.

That supply moves through the Strait of Hormuz. With the Strait closed, Australia’s primary urea supply corridor has been effectively severed.

Prices for granular urea at Australian import terminals have risen from approximately $870 per tonne in late February 2026 to between $880 and $1,000 per tonne as of mid-March, with some spot deals for uncommitted volumes reportedly clearing above $1,200 per tonne.

Global urea prices are up approximately 50 percent in three weeks. That is not a market adjusting through normal price signals. That is a market reflecting the abrupt removal of supply.

Timing makes the situation more structurally acute. April through June is Australia’s winter cropping window. Wheat, barley and canola require nitrogen fertiliser applied before or at seeding.

Growers need approximately 1.2 million tonnes of urea in this period. Current stocks, without meaningful resupply, are expected to be exhausted by mid April. The window between now and that exhaustion is narrow.

It is being partially filled by diverted Southeast Asian supply and by precautionary purchasing from distributors who are anticipating further tightening.

Some bulk suppliers have already moved to committed-volume-only sales, meaning spot availability for farmers without pre-existing supply agreements has effectively disappeared in several markets.

Some farmers are pivoting to ammonium sulphate as a urea substitute. This is a rational short-term response given the price differential.

The less examined complication is that Australia’s ammonium sulphate imports are heavily concentrated from China.

If that supply corridor encounters its own disruption, whether from logistics constraints, trade tensions or China’s own domestic supply prioritisation, the substitution pathway closes quickly.

Australia would be trading one geographic concentration risk for another without having resolved the underlying structural exposure.

There are approximately 229,000 tonnes of urea currently in transit to Australia.

Around 119,000 tonnes are sailing from Southeast Asian origins, primarily Brunei, Malaysia and Indonesia, with a voyage time to the east coast of approximately two to three weeks.

Around 165,000 tonnes are coming from Saudi Arabia and the UAE. Those Gulf cargoes may face difficulty clearing Hormuz depending on how the conflict develops in the coming fortnight. The Southeast Asian tonnage provides a meaningful near-term buffer. It is not a structural solution.

6.0 The Yara Pilbara Factor.

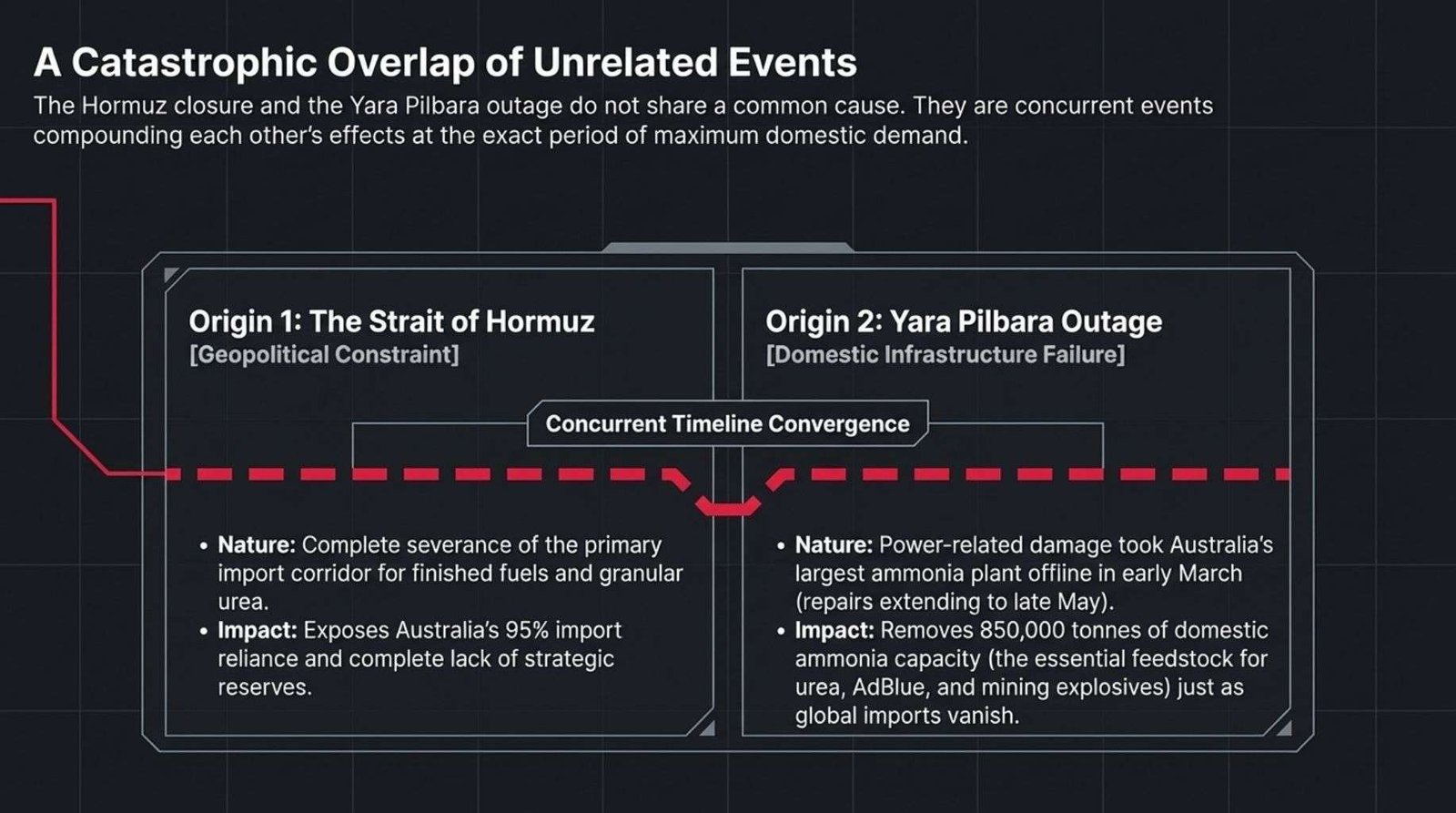

Australia’s largest ammonia plant, operated by Yara at the Pilbara site in Western Australia, has been offline since early March due to power-related equipment damage. The repair timeline extends to at least late May.

Ammonia is the primary feedstock from which urea is synthesised. Without ammonia you cannot make urea, and without urea you cannot make AdBlue or granular fertiliser.

The Yara Pilbara facility produced approximately 850,000 tonnes of ammonia in the previous year. The next largest domestic plant produced around 255,000 tonnes. The concentration of Australia’s domestic ammonia capacity in a single facility is extraordinary, and its failure at this specific moment is as damaging as any single event in the broader crisis.

The plant’s outage intersects with three distinct downstream supply chains simultaneously. The first is granular urea for agricultural fertiliser application during the winter cropping window.

The second is urea solution for AdBlue manufacturing, which feeds directly into the operability of Australia’s commercial freight fleet.

The third is technical ammonium nitrate, the primary blasting explosive used in Pilbara iron ore mining operations.

If technical ammonium nitrate supply tightens materially, the mining sector, which generates a significant portion of Australia’s export revenue and therefore its fiscal position, faces a production constraint that has nothing to do with commodity prices or demand conditions.

A production slowdown in the Pilbara iron ore mines would shift the current crisis from being primarily a cost-of-living and transport issue into a constraint on national income. That is a different and more serious category of consequence.

The Yara outage and the Hormuz closure are not related events. They did not arise from a common cause.

They are concurrent events that compound each other’s effects at exactly the period of maximum agricultural demand.

The overlap is severe and the timing is, from a supply chain management perspective, about as unfavourable as could be constructed.

7.0 AdBlue and the Mechanical Hard Stop in Australia’s Freight Fleet.

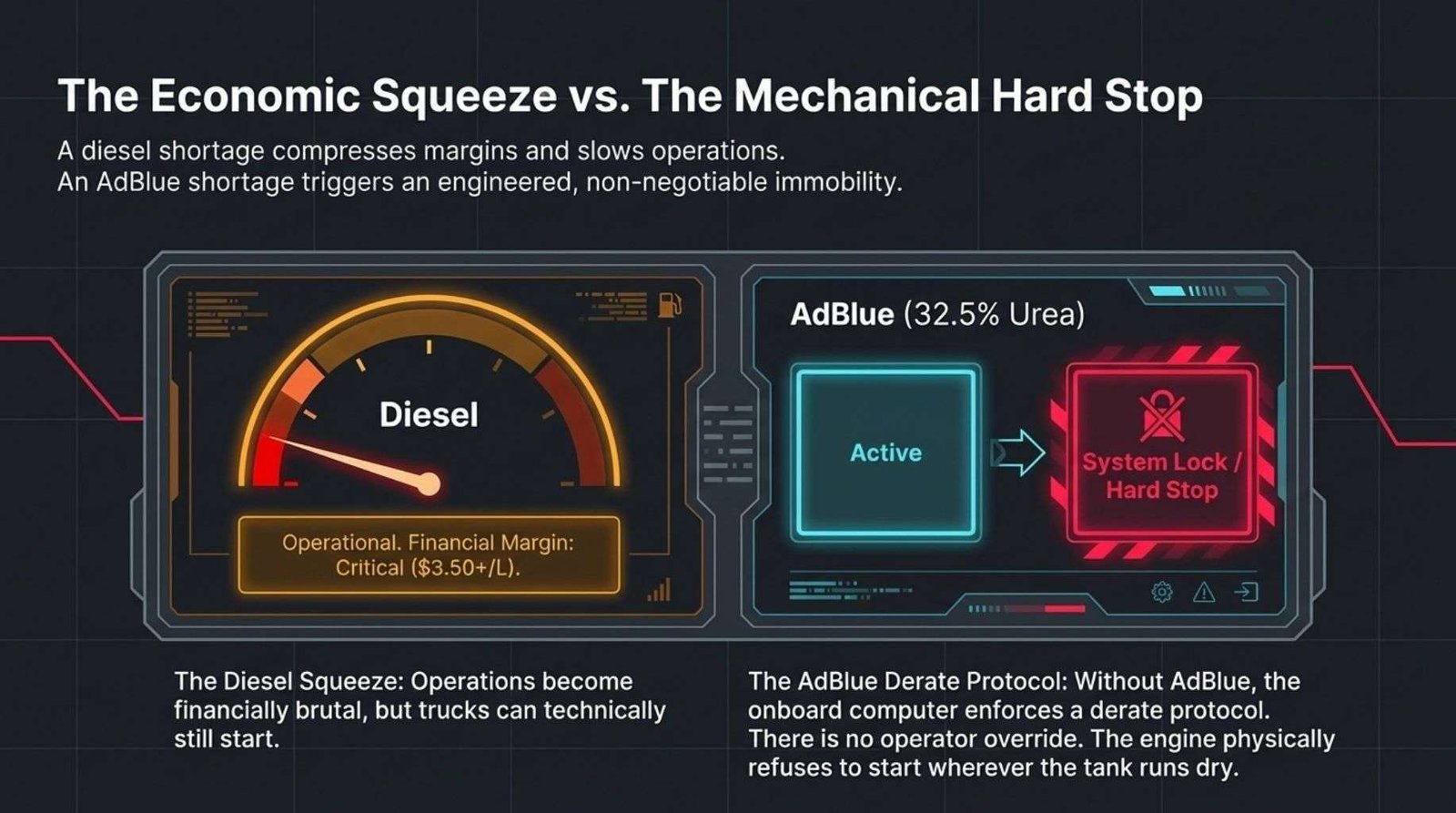

AdBlue is a solution of 32.5 percent urea in deionised water. It is injected into the exhaust treatment systems of Euro 5 and Euro 6 diesel engines, which constitute the overwhelming majority of Australia’s commercial freight vehicle fleet, as well as modern agricultural machinery, buses, emergency service vehicles and many mine site equipment units.

The injection process converts nitrogen oxide emissions to nitrogen and water through selective catalytic reduction.

This is not optional equipment in the vehicles that carry it. It is a mandated emissions control system embedded in the engine management software at the point of manufacture, and it cannot be removed without voiding compliance.

The engineering reality is precise and non-negotiable. If an AdBlue tank runs empty, the engine’s on-board computer activates a derate protocol that progressively limits engine power output.

If the fluid is not replenished promptly, the system escalates to a condition where the engine will not start on the next ignition attempt.

There is no operator override. There is no bypass procedure available under standard operating conditions.

A truck driver who runs out of AdBlue on the Hume Highway between Sydney and Melbourne does not limp to the next service centre at reduced speed. Their vehicle stops, and it does not restart until AdBlue is sourced and filled.

This is the mechanical reality that makes the AdBlue dimension of the urea crisis qualitatively different from a fuel price increase or a general supply reduction.

A diesel price increase at $3.50 per litre is painful and compresses margins.

An AdBlue shortage does not compress margins. It stops vehicles physically, without warning, at whichever location they happen to be when the tank empties.

The national freight network does not slow down gradually under AdBlue depletion. Specific vehicles, on specific routes, stop.

Retail AdBlue rationing has begun at some outlets. Industry stocks are currently described as adequate, but that adequacy is conditional on urea supply continuing at close to current pace.

If urea for AdBlue production runs short before agricultural season demand is resolved, a formal allocation decision between the two competing uses must be made. That decision has not been made publicly.

The freight industry has communicated its concern to government directly. The public framing of the issue has not yet reflected the mechanical finality of what happens when AdBlue supply reaches zero.

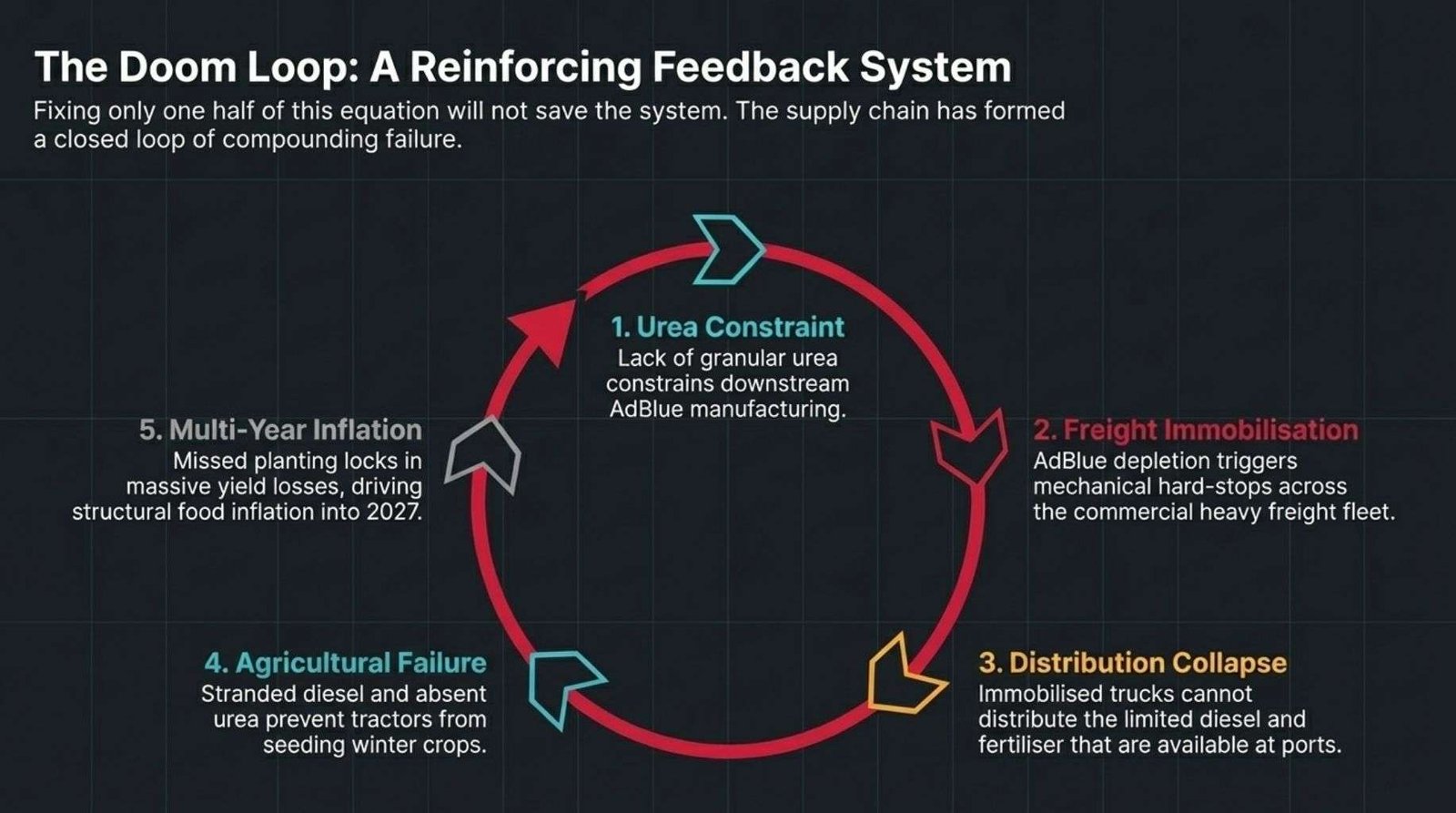

8.0 The Reinforcing Loop Between Fuel and Urea.

The two crises do not merely coexist. They form a loop with the potential to accelerate. Diesel shortages put pressure on agricultural logistics, including the fuel required to operate tractors, header machines and grain transport.

Urea shortages put pressure on winter crop yields, which affects food production volumes six to twelve months from now.

AdBlue shortages, as a direct consequence of urea tightness, threaten to immobilise the freight trucks that would otherwise move food from farms to processors and from processors to supermarkets.

Also, diesel engine immobilisation through AdBlue depletion is a freight disruption that compounds the original diesel shortage by making the logistics system less able to function even with the diesel volumes it does have access to. The multi-year dimension of this loop deserves direct attention. Urea not applied to winter cropping ground in April and May 2026 does not have a remedial equivalent available later in the year.

Nitrogen deficiency at planting cannot be corrected after seeding without significant yield loss. If urea cannot reach key growing regions of Western Australia, South Australia, Victoria and New South Wales within the seeding window, the yield outcome for the 2026 harvest will be measurably reduced.

Wheat and barley yields under nitrogen-deficient conditions can fall by 30 to 50 percent relative to adequately fertilised crops, depending on soil type, growing season rainfall and variety.

Reduced domestic grain production flows into elevated food prices at the retail level, persisting well beyond any resolution of the Hormuz situation.

The farm-gate input decision of the next six weeks will shape what consumers pay at the supermarket through 2027.

This is the multi-year tail of the crisis. It is not speculative. It is a direct consequence of the agricultural calendar and basic crop physiology.

Even if the Iran conflict resolved tomorrow and the Strait reopened next week, urea not applied in April 2026 cannot be applied retroactively.

9.0 A Comparison of Current and Projected Positions.

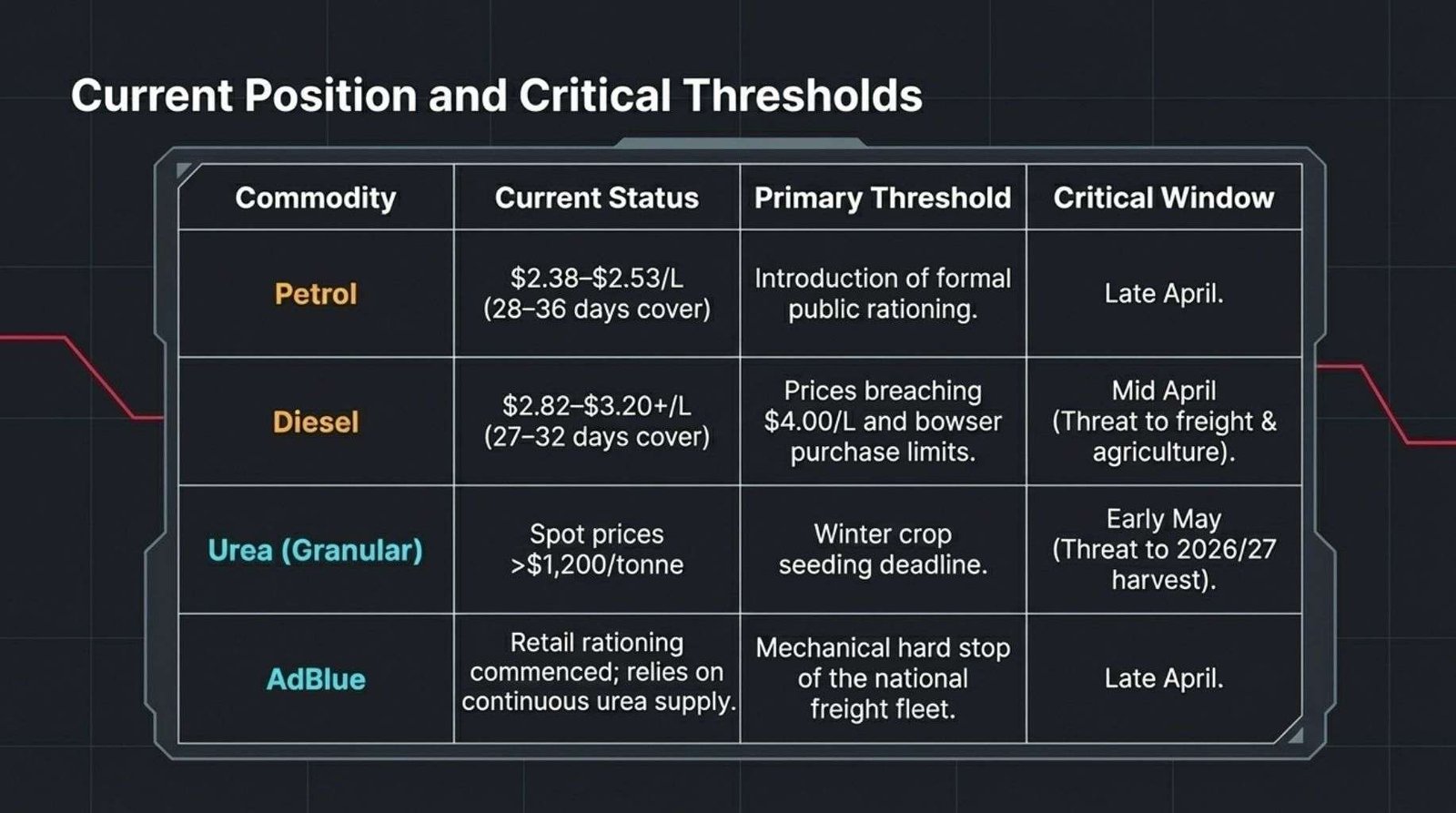

1. Petrol

a. Current status: Prices are sitting between $2.38 and $2.53 per litre, with national reserves estimated at roughly 28 to 36 days of cover.

b. Primary threshold: The major trigger point is the introduction of formal rationing, which would only occur if supply tightens further or panic buying accelerates.

c. Critical window: Without new supply, petrol becomes a national problem by late April.

2. Diesel

a. Current status: Diesel is trading between $2.82 and $3.20+ per litre, with about 27 to 32 days of cover remaining.

b. Primary threshold: The key warning signs are diesel reaching $4.00 per litre and the introduction of purchase limits at the bowser.

c. Critical window: Diesel becomes critically constrained by mid‑April, especially for freight, agriculture, waste collection, and emergency services.

3. Urea (Granular Fertiliser)

a. Current status: Domestic prices are between $880 and $1,000 per tonne, with spot prices already exceeding $1,200 per tonne.

b. Primary threshold: The decisive point is the winter crop seeding deadline, when farmers must apply nitrogen to maintain yields.

c. Critical window: Urea becomes a national agricultural constraint by early May, with consequences flowing into the 2026–27 harvest.

4. AdBlue (Diesel Exhaust Fluid)

a. Current status: Retail rationing has begun in some regions as suppliers struggle to secure automotive‑grade urea.

b. Primary threshold: The critical threshold is a mechanical stop of the freight fleet — modern diesel engines derate and shut down without AdBlue.

c. Critical window: AdBlue becomes a transport‑system threat by late April, entirely dependent on urea availability.

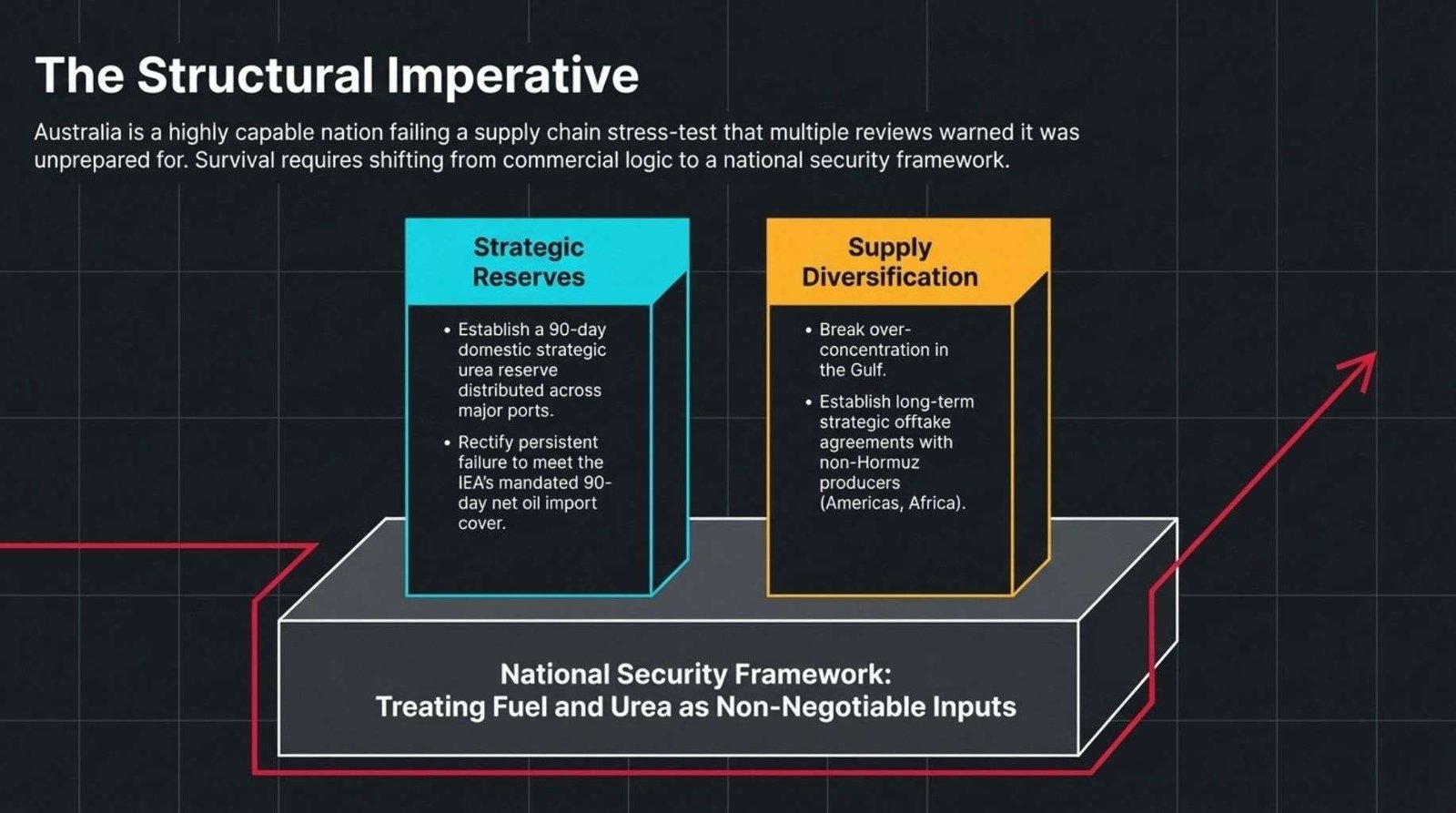

10.0 What the Policy Response Should Include.

Australia’s immediate operational levers are constrained but not exhausted.

The government has already acted on fuel quality standards, emergency reserve releases and anti-gouging enforcement.

Several additional steps deserve public framing.

The priority allocation question for urea requires a formal answer now. AdBlue production and agricultural fertiliser use are competing for the same feedstock.

A publicly stated priority framework, even one that involves real trade-offs, is more useful than managing the tension informally until one sector runs short without warning.

Prioritising urea for AdBlue production for a defined 30-day window would keep the freight fleet operational while alternative fertiliser sources are pursued.

The consequence is measurable pressure on winter crop nitrogen applications. That trade-off is real and specific: keeping trucks running means accepting some reduction in the completeness of the winter fertiliser program for 2026.

It is also a decision that benefits from being made explicitly, with appropriate support mechanisms for the agriculture sector, rather than being deferred until the outcome is forced by supply depletion.

A temporary reduction or suspension of the fuel excise, currently approximately 50 cents per litre, would provide direct and immediate relief to transport operators whose margins are being compressed toward the point where continued operations become financially unviable.

The cost of that measure to the federal budget is real and finite.

The cost of allowing medium-sized freight operators to become insolvent during a supply crisis is harder to quantify but potentially larger in scale and more persistent in its consequences for supply chain capacity.

Transparent triggering criteria for escalating from soft to hard rationing would reduce planning uncertainty for businesses that need to make operational decisions now.

Linking formal rationing measures to published and measurable thresholds, such as a specific number of days of cover for diesel in priority sectors, gives industry a planning horizon.

Reactive announcements without lead time are more disruptive than pre-announced frameworks even when the news in both cases is the same.

The medium-term structural response to this situation should begin now rather than after the immediate pressure eases.

Australia’s national fuel reserve position has been assessed in multiple independent reviews as marginal relative to comparable OECD nations.

The IEA recommends member countries hold 90 days of net oil import cover. Australia has persistently fallen short of that target, and the current situation is a direct operational consequence of that gap.

The case for a strategic urea reserve, equivalent in concept to a fuel reserve and sized at a minimum of 90 days of domestic consumption, has appeared in policy discussions for years.

Fertiliser security reviews commissioned after the 2021 global urea price shock recommended exactly this.

The current crisis is the scenario those reviews described.

Establishing a domestic strategic urea reserve, held at distributed locations near major port facilities in Fremantle, Geelong, Brisbane and Port Adelaide, would insulate Australia’s agricultural and freight sectors from the next Hormuz disruption, the next major export restriction from a key supplier, or the next domestic ammonia plant failure.

All three of those events have now occurred within a 24-month window. The argument for the reserve no longer needs to be made hypothetically.

Supply diversification is a longer-term structural project that requires policy commitment. Australia’s urea import base is over-concentrated in the Gulf.

Southeast Asia provides roughly a third of current imports but has limited spare capacity and its March allocations are largely committed.

The Americas and Africa both have urea production infrastructure that is not subject to Hormuz risk.

Long-term offtake agreements with non-Gulf producers, structured as strategic supply contracts rather than purely spot or annual commercial arrangements, would materially reduce exposure to any single chokepoint.

That requires treating fertiliser and AdBlue feedstock as national security inputs. The evidence that they are national security inputs is now plainly visible.

11.0 The Indicators Worth Watching.

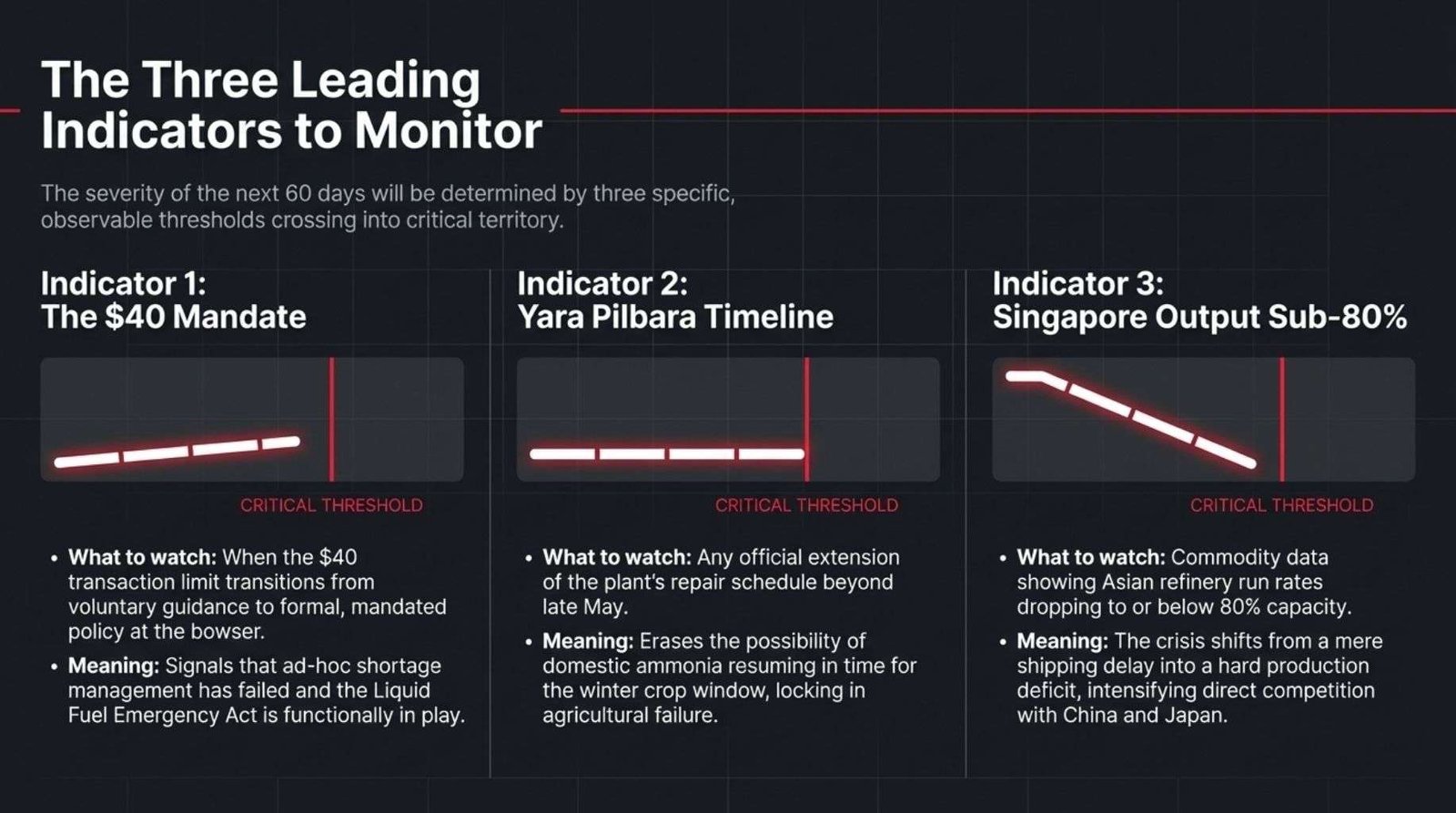

Three specific observable thresholds will determine how the situation develops over the next 30 to 60 days.

The first is whether the $40 transaction limit moves from a publicly discussed option to a formally mandated policy at individual bowsers or nationally.

That shift signals that voluntary demand suppression has been judged insufficient and that formal rationing has been accepted as the available instrument. It is also the point at which the government has made the calculation that managing a known rationing system is preferable to managing the unpredictable dynamics of ad hoc shortage.

The second is whether the Yara Pilbara repair timeline extends beyond its current late-May estimate.

A blow-out in that schedule removes the prospect of partial domestic ammonia supply resuming before the critical winter cropping window closes entirely.

It extends the period of ammonium nitrate pressure on the Pilbara mining sector and narrows the already limited domestic buffer for AdBlue feedstock production.

The third is the published output level from Singapore’s major refinery complexes. Singapore refinery run rates are tracked by commodity data providers and material changes appear in reporting within days.

If Singapore refinery runs fall to or below approximately 80 percent of normal capacity due to reduced crude availability from the Middle East, the supply constraint shifts from a shipping issue to a production issue.

Fewer barrels exist globally. Competition for those barrels intensifies from buyers who are larger and closer to the refineries than Australia.

The ability to secure replacement supply from non-Hormuz routes diminishes because other buyers are attempting exactly the same sourcing shift simultaneously.

12.0 What the Current Position Means for Australia.

Australia is a well-resourced, technically capable and administratively functional country facing a supply chain stress test that its infrastructure was not designed to pass without difficulty. That is an accurate description of the structural position. It is not a condemnation and it is not a reassurance.

The fuel situation is serious but not at the point of system failure.

Stocks exist at a national level. Alternatives are being sourced. The government is deploying available tools.

The urea situation carries more structural risk because the agricultural demand window is narrow and non-recoverable, and because the AdBlue dependency creates a freight vulnerability with hard mechanical limits rather than the graduated financial pressures that characterise a fuel price increase.

Diesel users who depend on their vehicles for work should maintain operational reserves without surplus hoarding, monitor their AdBlue supply position actively and stay informed on the policy decisions that will govern priority allocation in the weeks ahead.

Farmers in the winter cropping regions should be in active dialogue with agronomists about substitution options and application timing given constrained urea availability. Freight operators should be communicating the AdBlue constraint directly to government if they have not already done so, and their industry associations should be pressing for the formal allocation framework to be decided rather than deferred.

The observation worth carrying beyond the immediate situation is this: Australia has known for at least two decades that its fuel self-sufficiency is inadequate and its fertiliser supply chain is exposed. Multiple independent reviews have documented both vulnerabilities in precise terms.

The 2019 emergency planning exercise identified exactly the failure modes that are now observable in practice.

The current situation is not a surprise to anyone who engaged seriously with those policy documents.

It is a scenario that was identified, assessed and not resolved.

The road ahead from here is manageable. It requires clear decisions, transparent public communication about what the actual thresholds are, and a willingness to accept that some short-term costs are the price of long-term supply resilience.

The Australian government has managed supply-side economic shocks before, and the institutional capacity to escalate through the available policy levers exists. The question is whether the current situation will generate the sustained political attention required to produce structural change, or whether the response will, as has happened after previous reviews, produce recommendations that are acknowledged and deferred.

What the next five years look like depends on whether Australia treats fuel and urea as strategic national security inputs or reverts, once the immediate pressure eases, to the commercial logic that produced the current exposure.

That question does not have a policy answer yet. It has a political will question inside it that only Australians and their elected representatives can resolve.

13.0 Conclusion.

Australia confronts a foreseeable supply chain crisis in fuel and urea, rooted in Hormuz dependency and inadequate reserves, now manifesting in economic threats from freight halts to crop failures.

Immediate policy must prioritize urea allocation, suspend excises, and set rationing triggers, while building 90-day strategic stocks and diversifying sources to avert recurring vulnerabilities.

Resilient supply chains demand treating these inputs as national security priorities, converting this stress test into enduring reforms.

14.0 Verify the Facts Yourself.

This articles draws from publicly available data and reporting as I could find 25th March 2026.

Key claims are supported by primary sources including government statements from Energy Minister Chris Bowen, fuel reserve and shortage statistics,

Hormuz closure impacts, Yara Pilbara outage details, and urea/AdBlue supply pressures.

If you disagree or would like to check specifics, review these outlets directly, facts evolve with new developments every couple of hours as everyone would appreciate.

Global chokepoint and energy flows:

1. U.S. Energy Information Administration (EIA) – World Oil Transit Chokepoints (Strait of Hormuz)

2. International Energy Agency (IEA) – Oil Market Report (monthly data on flows and chokepoints)

3. BP Statistical Review of World Energy (now Energy Institute) – global oil and LNG trade data

4. UN Conference on Trade and Development (UNCTAD) – maritime chokepoint and shipping analysis

5. Lloyd’s List Intelligence – shipping lane congestion and insurance risk reporting

Hormuz strategic importance:

1. EIA – The Strait of Hormuz is the world’s most important oil transit chokepoint

2. Congressional Research Service (CRS) – reports on Persian Gulf energy flows

3. International Maritime Organization (IMO) – Traffic Separation Scheme details

4. UK Defence Science and Technology Laboratory / MOD briefings on maritime chokepoints

Australia fuel dependency and reserves:

1. Australian Government – Department of Climate Change, Energy, the Environment and Water (DCCEEW) – Australia’s Liquid Fuel Security Review (2019)

2. Australian Institute of Petroleum (AIP) – Downstream Petroleum Industry Report

3. Australian Bureau of Statistics (ABS) – Energy Supply and Use, Australia

4. IEA – Australia Energy Policy Review (includes stockholding levels vs 90-day requirement)

5. ACCC – Petrol Monitoring Reports (pricing and supply trends)

Refining and import structure (Asia linkages):

1. International Energy Agency – refinery sourcing and regional crude flows

2. S&P Global Commodity Insights (Platts) – Asian refinery utilisation and crude sourcing

3. Wood Mackenzie – Asia-Pacific refining outlooks

4. Singapore Energy Market Authority – refining hub data

Diesel dependence and economic role:

1. Australian Bureau of Infrastructure and Transport Research Economics (BITRE) – freight and fuel usage

2. National Transport Commission (NTC) – heavy vehicle fleet composition

3. Australian Trucking Association (ATA) – diesel reliance and freight impacts

Urea, fertiliser, and AdBlue:

1. ABARES – Australian fertiliser use and agricultural input reports

2. Fertilizer Australia – import dependence and supply chains

3. CRU Group – global urea market analysis

4. World Bank – fertiliser price indices

5. Incitec Pivot Ltd – Australian fertiliser supply chain insights

6. Australian Government (2022) – AdBlue Taskforce and urea supply reports

Yara Pilbara and ammonia/urea linkage:

1. Yara International – Pilbara plant production data and disclosures

2. Western Australian Government – industrial production and ammonia capacity

3. Resources and Energy Quarterly (Office of the Chief Economist, Australia)

Strategic reserves and policy frameworks:

1. IEA – 90-day stockholding obligation documentation

2. Australian Government – Liquid Fuel Emergency Act 1984 and 2019 Emergency Guide

3. Productivity Commission – infrastructure and supply chain resilience reports