Strengthening Australia’s National Resilience

Disclaimer.

This article is my personal analysis of Australia’s fuel, fertiliser and broader national resilience posture.

It is not technical, legal, financial, political, financial, business or military advice. Any policy, investment, or operational decisions should be based on detailed specialist analysis, formal risk assessments and relevant statutory and regulatory frameworks.

Thoughts, views, opinions and ideas expressed are those of the author only.

The information that follows is not a crisis narrative; it’s a structural one.

Top 5 takeaways.

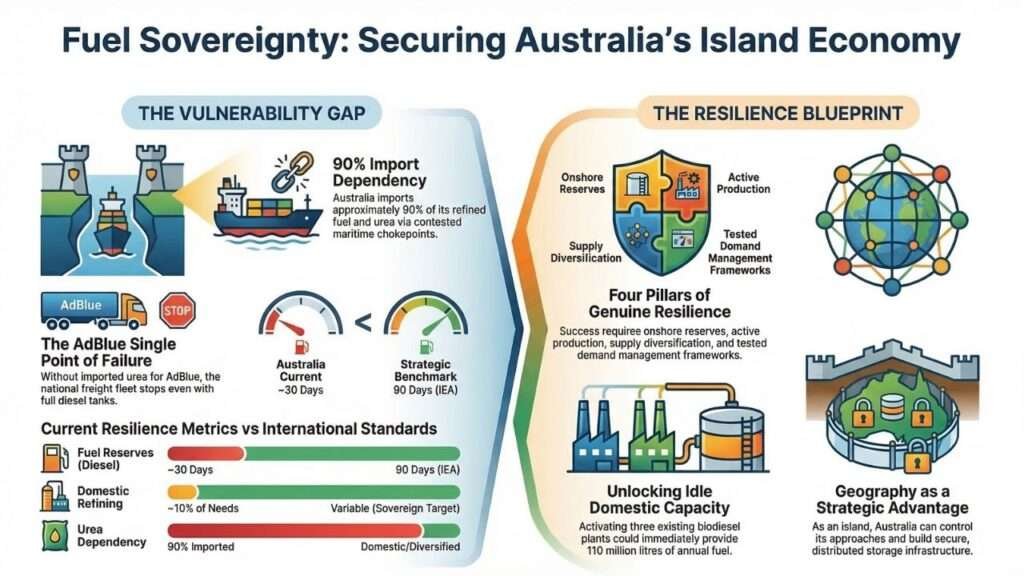

1. Australia’s vulnerability is a governance failure, not resource scarcity. Biodiesel plants sit idle at 10-15% capacity while we export feedstocks.

2. Urea > Diesel: AdBlue shortages immobilise the freight fleet even with full tanks. 90% import reliance through Hormuz = single-point failure.

3. 30 days reserves vs IEA 90-day benchmark = no buffer for 60-day disruptions. Regional Australia (farming, remote communities) fails first.

4. LPG infrastructure dismantling forfeits diesel reallocation to priority sectors (agriculture, defence) while urban fleets consume freely.

5. Our Island geography is an advantage when paired with domestic production + reserves. Current policy treats resilience as an overhead cost, not a design requirement.

Overview.

Australia’s structural vulnerability to fuel and fertiliser disruption is the product of deliberate policy choices rather than resource scarcity.

The nation operates with roughly 30–36 days of refined fuel coverage depending on product, far below the 90‑day stockholding obligation required of members of the International Energy Agency (IEA).

Australia remains heavily import‑dependent, sourcing around 90% of its refined liquid fuels from overseas markets, much of it transiting vulnerable maritime chokepoints such as the Strait of Hormuz.

Domestic capability has simultaneously contracted. Australia now operates only two refineries; Geelong and Lytton, this leaves our country structurally dependent on imported diesel, petrol and jet fuel.

While biofuel capacity exists, it remains marginal within the national fuel mix.

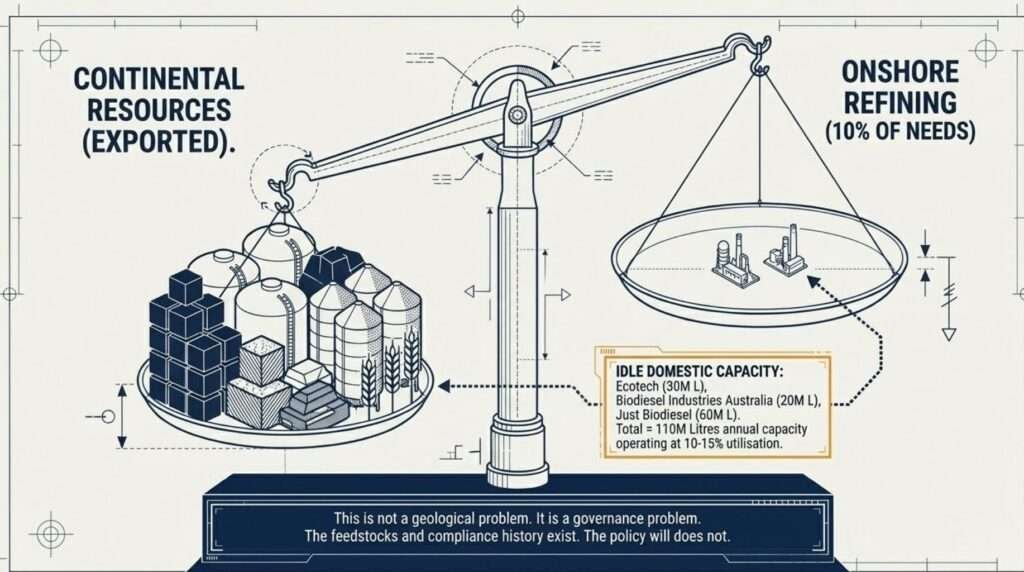

Biodiesel facilities with an estimated 110 million litres of annual capacity continue to operate well below potential utilisation, even as Australia exports large volumes of feedstocks such as canola oil and tallow that could support sovereign production.

The resulting configuration reflects long‑term industrial and policy choices rather than geological limits.

Each time there is a Middle East conflict, it has the potential to create a disruption to shipping through the Strait of Hormuz.

Now in particular with 2026, this has happened and it’s happened in a very big way, it has exposed the severe fragility of this model and we can only hope we decide to do better with the future.

Fuel prices have surged and governments across the world have coordinated strategic stock releases.

Australia has joined this effort by releasing roughly 762 million litres (about five million barrels) from domestic emergency reserves, around 20% of its minimum stockholding obligation inventory, to stabilise supply chains and regional fuel availability. However, despite this intervention, structural vulnerabilities remain visible. Diesel supply is critical for freight, agriculture, mining and defence logistics, while an additional urea shortage (fertilizer and Adblue), are also exposed to global supply shocks and are of equal concern.

Agricultural inputs and diesel distribution networks are tightly coupled, meaning that disruptions in shipping, refining or fertiliser production can cascade across food production and transport simultaneously.

Regional distribution constraints have already produced localised shortages and prompted emergency measures such as temporary relaxation of fuel quality standards to maintain supply continuity.

Geography should in principle provide strategic advantages for an island continent capable of controlling its maritime approaches.

Instead, the current system prioritises supply‑chain efficiency and global market integration over redundancy and resilience.

True fuel resilience rests on four interlocking pillars: onshore reserves, domestic production capability, diversified supply routes, and coordinated demand management during crises.

Peer nations such as Japan maintain extensive strategic petroleum reserves and codified emergency allocation protocols to manage disruptions.

Australia continues to lag behind these benchmarks. Even with recent increases in stock levels, national reserves remain well below the IEA benchmark, and the country has struggled for more than a decade to meet the treaty obligation requiring members to hold oil stocks equivalent to 90 days of net imports.

Recent federal initiatives, including fuel security payments for domestic refineries and the expansion of the Minimum Stockholding Obligation, represent incremental progress, but they do not yet constitute a fully integrated fuel security strategy. Major industrial projects intended to improve fertiliser sovereignty, such as large‑scale domestic urea production facilities, remain delayed into the latter part of the decade.

A practical policy agenda nevertheless exists.

Over the next 0–3 months, Australia could rapidly increase supply resilience by activating idle biodiesel capacity through targeted production subsidies and temporary B10 blending mandates for heavy‑duty transport. At the same time, establishing a strategic inland urea reserve of approximately 180 days would buffer agricultural supply chains against external fertiliser shocks.

Within 3–6 months, policy could stabilise and protect LPG distribution networks while incentivising urban fleet conversions away from diesel where practical, freeing critical liquid fuel supply for freight, agriculture and emergency services.

Within 6–12 months, renewable diesel and biodiesel production could be co‑located at existing refinery sites, leveraging existing logistics infrastructure and programs such as the $1.1 billion Cleaner Fuels Program to accelerate domestic liquid fuel capability.

Beyond 12 months, Australia could institutionalise fuel sovereignty through mandatory annual fuel‑security audits, integrated fertiliser‑energy planning, and long‑term strategic capability frameworks that treat liquid fuel supply as critical national infrastructure rather than a purely commercial commodity.

The underlying lesson of the current crisis is simple: fuel vulnerability in Australia is not a resource constraint but a systems‑design problem.

Correcting it requires moving beyond short‑term market optimisation toward deliberate national capability planning.

Table of Contents.

1.0 Introduction: Australia’s Structural Vulnerability

1.1 A Continent Defined by Isolation

1.2 A High Dependency Economy

1.3 A Paradox of Abundance

1.4 A System with Single Points of Failure

2.0 Defining National Resilience.

3.0 The Structural Pattern of Disruption

4.0 The Fuel System Australia Built and What It Cannot Do

5.0 An Island Nation With Continental Resources

6.0 Maritime Dependency and the Geography of Risk

7.0 Fertiliser, Urea and the Food System Connection

8.0 The Resilience Gap: Where Australia Stands

9.0 LPG: A Strategic Asset Without a Strategy

10.0 What Genuine Resilience Requires

11.0 A Practical Agenda: Four Horizons of Action

11.1 Immediate Horizon (0–3 Months): Unlocking Idle Capacity

11.2 Medium Horizon (3–6 Months): Structural Reinforcement

11.3 6–12 Month Horizon: Domestic Production Rebuild

11.4 12+ Month Horizon: Institutionalising Fuel Sovereignty

12.0 The Political Economy of Urgency

12.1 Scenario Analysis: A 60 Day Supply Disruption

13.0 Conclusion

14.0 Bibliography

1.0 Introduction: Australia’s Structural Vulnerability.

Australia’s vulnerability to global shocks is not sudden, accidental, or unforeseeable.

It is structural, cumulative and the direct result of policy, market and governance choices made over several decades.

Modern Australian life; fuel, food, freight, emergency services, construction, manufacturing and defence all relies on systems that are tightly coupled and increasingly exposed to external disruption. Understanding this vulnerability begins with geography, but it does not end there.

1.1 A Continent Defined by Isolation.

Australia is a vast island continent with no land borders, situated at significant distance from major population centres and industrial economies.

Its nearest neighbours lie across extensive maritime zones and every movement of goods or people requires aviation or shipping.

This physical separation shapes Australia’s trade patterns, supply‑chain dependencies and strategic posture.

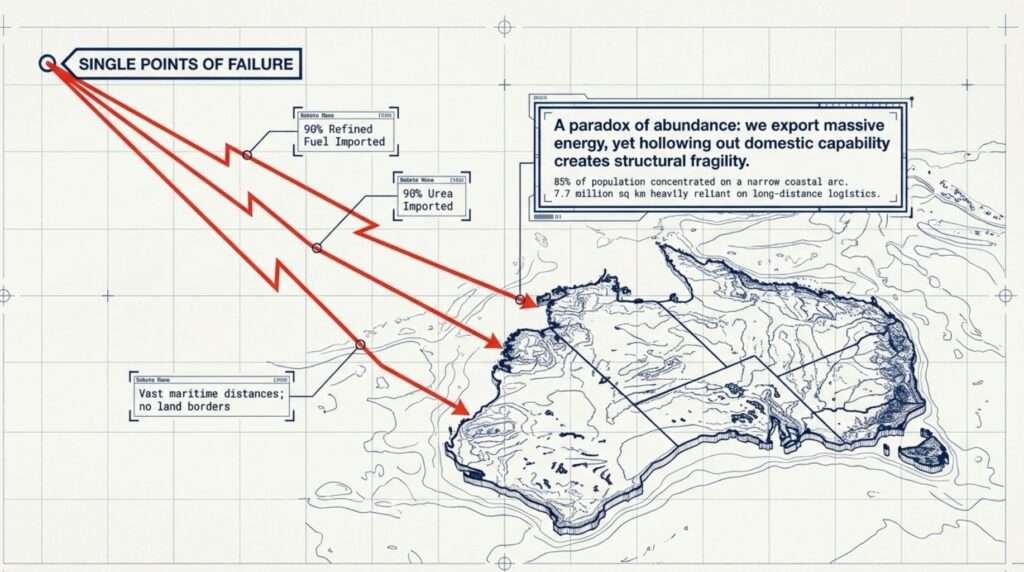

Although the continent spans roughly 7.7 million square kilometres, more than 85% of Australians live along a narrow coastal arc on the eastern, southeastern and southwestern seaboards.

The interior remains sparsely populated due to its arid climate and limited infrastructure. This settlement pattern reinforces the country’s reliance on maritime access, coastal infrastructure and long‑distance logistics.

Australia is bounded by three major oceans; the Indian, Pacific and Southern.

Even its closest approach to Asia is mediated by seas and archipelagos rather than contiguous land.

Our nation also administers remote external territories accessible only by extended sea or air routes.

Put it all together and our island nation’s features create a strategic environment in which connectivity, supply chains and national resilience are fundamentally shaped by geography.

1.2 A High Dependency Economy.

Over time, Australia has dismantled much of its domestic refining and fertiliser capability and replaced it with near‑total reliance on overseas production.

Today, the country imports approximately 90% of its refined fuel and 90% of its urea, with much of this supply transiting contested maritime chokepoints such as the Strait of Hormuz.

The shift from partial insulation to near‑total dependence has been deliberate, not accidental.

This dependence is particularly acute in the freight and agricultural sectors.

Diesel exhaust fluid (AdBlue), made from urea, is essential for modern diesel engines. A disruption to urea supply does not merely increase costs; it immobilises the national freight fleet.

Trucks can have full diesel tanks and still be unable to operate. Because fertiliser availability shapes planting decisions and yields, fuel security and food security are now tightly linked.

1.3 A Paradox of Abundance.

Australia’s vulnerability is not caused by resource scarcity.

The nation sits atop one of the world’s most significant energy and mineral estates, exporting LNG, coal, uranium, critical minerals and oilseed crops suitable for biofuels.

Yet domestic capability has withered: biodiesel plants sit idle, LPG infrastructure is declining, fuel reserves remain far below international benchmarks and domestic urea production is minimal until new projects come online. This is not a geological problem. It is a governance problem.

1.4 A System with Single Points of Failure.

The cumulative effect of geographic isolation, concentrated population, maritime dependence and hollowed‑out domestic capability is a system with multiple single points of failure.

A disruption to fuel refining, urea production, maritime chokepoints, or shipping schedules can cascade rapidly across freight, agriculture, emergency services and defence.

Australia’s resilience cannot be measured by storage statistics alone.

It must be understood as a design principle, one that requires onshore reserves, domestic production capacity, diversified supply routes and active demand management.

2.0 Defining National Resilience.

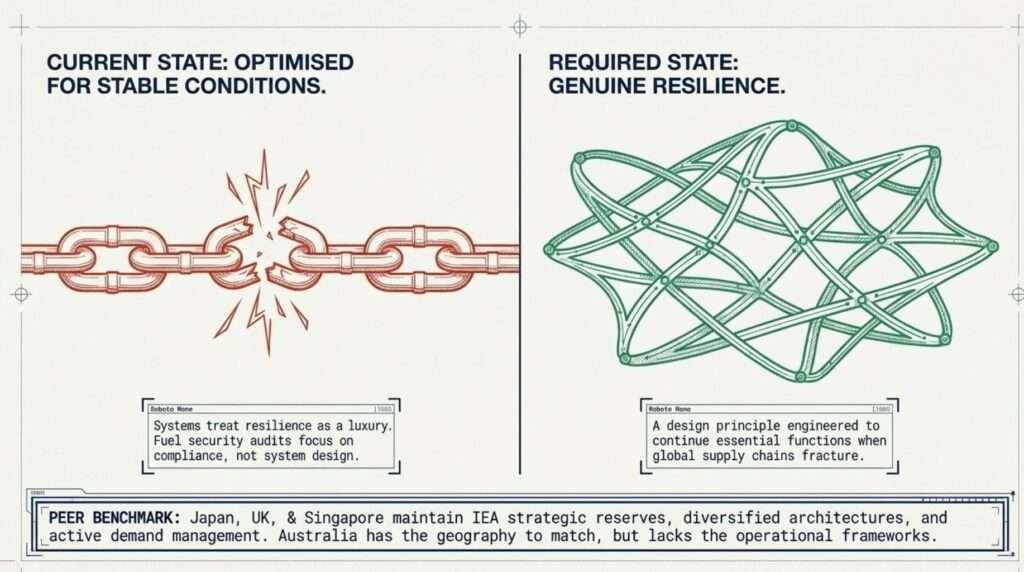

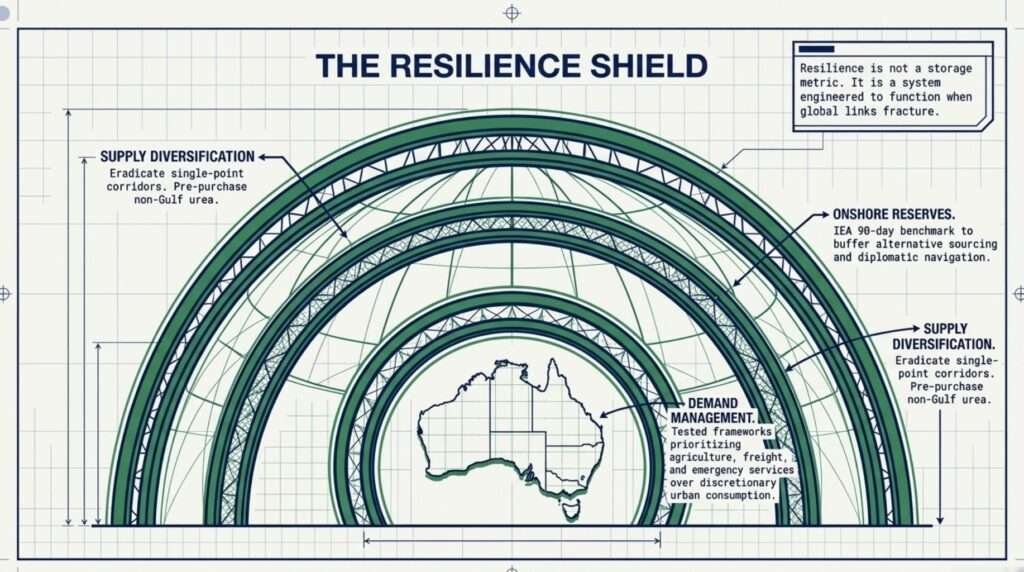

Resilience is not a storage metric or crisis response plan.

It’s a design principle, a system engineered to continue essential functions when global supply chains fracture.

For an island continent like Australia, genuine resilience requires four interdependent pillars:

1. Onshore Reserves: IEA 90-day benchmark (Australia: ~30 days). Time to source alternatives, adjust demand, navigate diplomacy.

2. Domestic Production Capacity: Activated facilities, not idling plants. Three biodiesel plants at 10-15% utilisation represent 110M litres of immediately available fuel.

3. Supply Diversification: No single chokepoint, source country, or supplier dominates. Multiple corridors, feedstocks, production methods.

4. Demand Management: Tested frameworks prioritising agriculture, freight, emergency services over discretionary urban consumption.

Island geography is an advantage when leveraged properly. Australia controls its approaches. It can build secure storage behind defended borders.

Distributed refining reduces single-point vulnerabilities. Remote communities become self-reliant hubs rather than import dependencies.

Current policy treats resilience as a luxury. Fuel security audits focus on compliance, not system design.

Biofuel mandates exist on paper but lack enforcement. LPG infrastructure dismantles without strategic replacement. Reserves remain conversation points, not mandated minimums.

The pattern is consistent: systems optimised for stable conditions, not disruption. Peer island nations; Japan, UK & Singapore, maintain strategic reserves at IEA levels, diversified supply architectures and active demand management protocols.

Australia has the resources and geography to match them. It lacks the frameworks that make those advantages operational.

This is the baseline Australia must meet before specific vulnerabilities (section 3.0 onwards) can be addressed systematically.

3.0 The Structural Pattern of Disruption.

The instability that periodically seizes global energy markets is not random. It follows a recognisable pattern and that pattern has a geography.

The Middle East sits at the intersection of several of the world’s most consequential energy corridors.

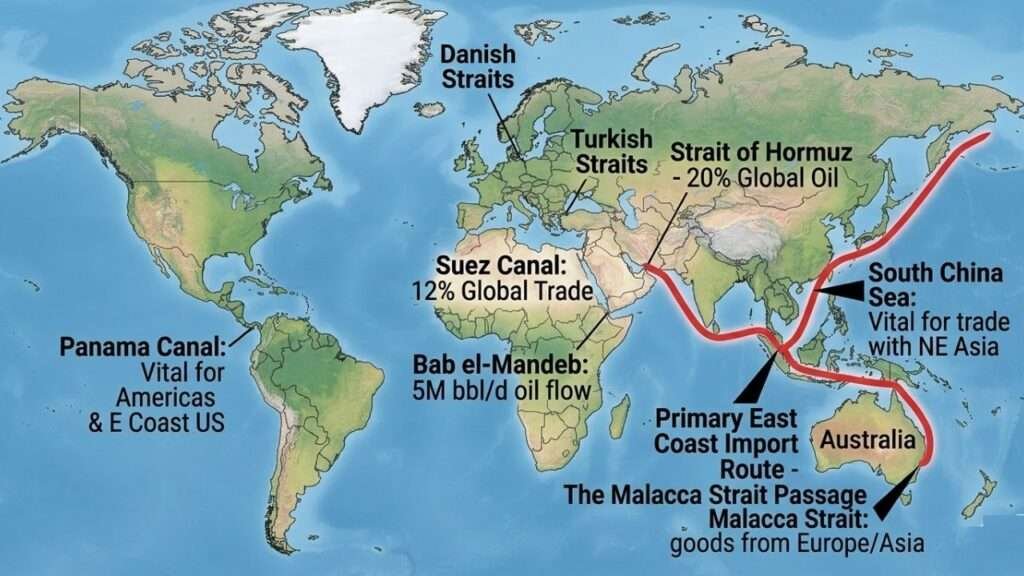

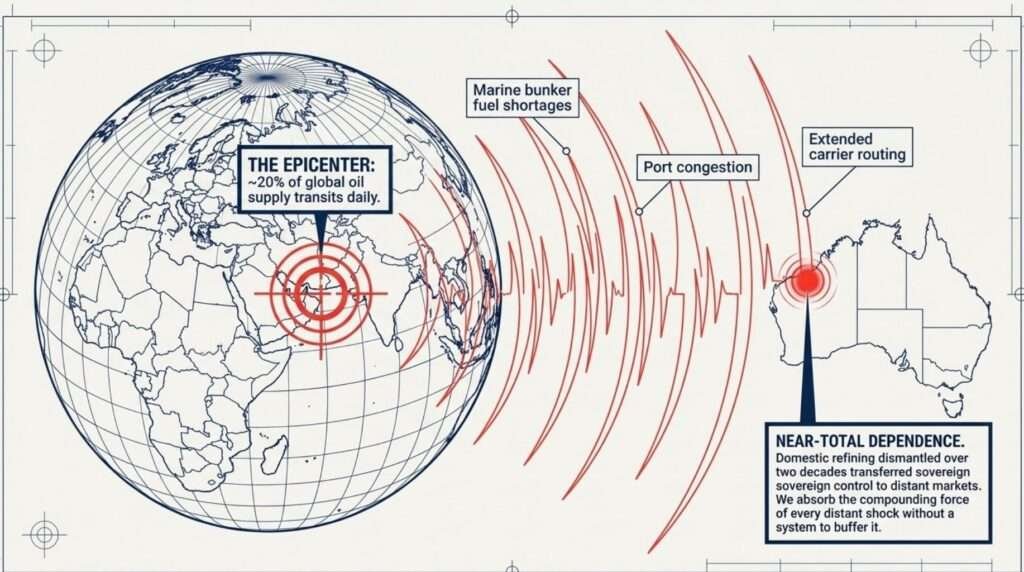

The Strait of Hormuz, through which approximately 20% of global oil supply transits daily, is one of the most strategically significant and geopolitically contested chokepoints on earth.

Regular flare-ups in the Gulf region, geopolitical tensions in key oil-producing corridors and the recurring threat of closure or restriction to these chokepoints have each, on multiple occasions, caused abrupt spikes in oil prices and disruptions to tanker routing.

The pattern is not new. What is new is Australia’s exposure to it.

As domestic refining capacity was progressively dismantled over the past two decades, the country moved from a position of partial insulation from global shocks to one of near-total dependence on them.

Each refinery closure transferred a layer of sovereign control to distant markets and foreign logistics operators.

Periodic disruptions to global shipping lanes compound the risk.

Marine bunker fuel shortages, port congestion, canal closures and attacks on commercial vessels have each demonstrated how quickly the world’s freight system can tighten.

When major carriers warn publicly that they cannot guarantee normal operations, the consequences for import-dependent economies are immediate and concrete: higher costs, longer lead times and supply gaps that cascade through every sector that depends on timely deliveries.

Australia has experienced the downstream effects of each of these disruptions. What it has not yet done is design a national system capable of absorbing them without a crisis response.

4.0 The Fuel System Australia Built and What It Cannot Do.

The current state of Australia’s fuel system is the cumulative result of deliberate choices, not geographic misfortune.

Seven refineries operated on Australian soil in the early part of this century. By the mid-2020s, two remained: Viva Energy’s Geelong facility and Ampol’s Lytton refinery in Brisbane.

The closures were driven by high operating costs, ageing infrastructure, the economics of competing against large Asian refineries and a policy environment that treated domestic refining as a cost centre rather than a strategic asset.

The consequence is that Australia now imports roughly 90% of its refined fuel.

That fuel travels on tankers that pass through maritime corridors subject to periodic disruption, is stored in facilities that hold a fraction of the reserves recommended by the International Energy Agency and is distributed through a logistics network that has very limited capacity to absorb sudden demand spikes or supply interruptions.

The International Energy Agency recommends that member nations maintain the equivalent of ninety days of net oil imports in strategic reserves.

Australia’s reported reserve levels, described at various points as the highest in fifteen years, sit at approximately one third of that benchmark.

A record low watermark is not a resilience position; it is a demonstration of how far the system has been allowed to erode.

There is a further complication that the public debate rarely addresses with adequate seriousness.

Modern diesel engines in trucks, buses, agricultural machinery, generators and construction equipment cannot operate without diesel exhaust fluid, commonly known as AdBlue. Its key ingredient is urea.

Australia imports approximately 90% of its urea and a significant portion of those imports transit the Strait of Hormuz.

A disruption to urea supply does not merely raise costs; it physically immobilises the national freight fleet, regardless of how much diesel remains in storage tanks. The diesel tanks can be full and the trucks still stop.

This is the specific, actionable limitation that deserves far more attention than it receives in the national resilience conversation.

5.0 An Island Nation With Continental Resources.

The profound irony of Australia’s vulnerability is that it sits atop one of the world’s most remarkable energy resource estates.

Australia exports vast quantities of liquefied natural gas, coal, uranium and the critical minerals that underpin global clean energy supply chains.

It grows and exports canola, tallow, sugarcane and other oilseed crops that are the raw material of biofuels.

It produces liquefied petroleum gas from domestic gas basins and legacy refinery operations in quantities that exceed national transport demand, making it a net exporter. It has the land, the solar resource and the wind resource to generate renewable energy at industrial scale.

What Australia lacks is not the raw material for energy sovereignty.

It lacks the refining capacity, the storage infrastructure, the blending mandates and the policy frameworks that would convert those raw materials into domestic fuel security.

Three east-coast biodiesel plants currently operate at a fraction of their certified capacity. Ecotech Biodiesel in Brisbane holds thirty million litres per year of processing capacity.

Biodiesel Industries Australia in Newcastle holds twenty million litres. Just Biodiesel in Barnawartha, Victoria holds sixty million litres.

Together, they represent one hundred and ten million litres of annual production capability, using feedstocks that Australia currently exports for others to refine.

All three facilities are operating at around 10 to 15% utilisation.

The reason is straightforward: biodiesel is more expensive than imported mineral diesel and there is no robust national mandate or price support mechanism to close that gap.

The capacity exists. The feedstocks exist. The compliance history exists. The policy will does not.

That is not a resource problem. It is a governance problem.

6.0 Maritime Dependency and the Geography of Risk.

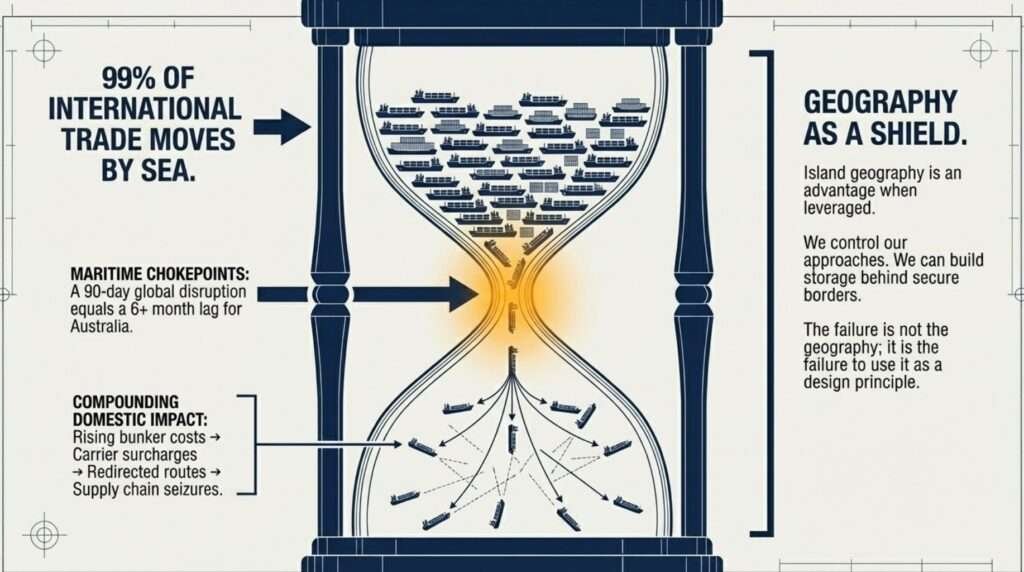

Up to 99% of Australia’s international trade moves by sea. That figure is not unusual for an island nation; it is the defining economic characteristic of island geography. What makes it significant in the current context is the concentration of risk within specific maritime corridors.

The Strait of Hormuz is the primary chokepoint through which Middle Eastern oil exports reach global markets. It is also the corridor through which a significant share of Australia’s urea imports travel.

Recurring instability in the region, geopolitical tensions in key oil-producing corridors and the documented pattern of regular flare-ups in the Gulf region mean that the risk of disruption is not hypothetical; it is a recurring feature of the operating environment.

When that corridor tightens, the consequences spread rapidly.

Marine bunker fuel costs rise, forcing carriers to impose surcharges that flow through to every imported good.

Major shipping companies redirect routes, adding days or weeks to transit times. Vessels queue outside congested ports. The supply chain tightens at every node simultaneously.

Australia’s geographic position at the southern end of several major shipping routes means that these effects arrive with a lag but with compounding force.

A disruption that affects global shipping for ninety days is not merely a ninety-day problem for Australia; it can represent a six-month or longer disruption to specific supply lines, particularly for goods that require temperature control, have limited shelf lives, or depend on just-in-time delivery schedules.

The counter-intuitive observation here is that Australia’s island geography, which appears to be a source of vulnerability, is actually a structural advantage for a nation serious about resilience. An island nation controls its own approaches. It can build storage infrastructure behind secure borders.

It can develop distributed refining and processing capacity that is not easily interdicted. The geography is not the problem; the failure to use it as a design principle is the problem.

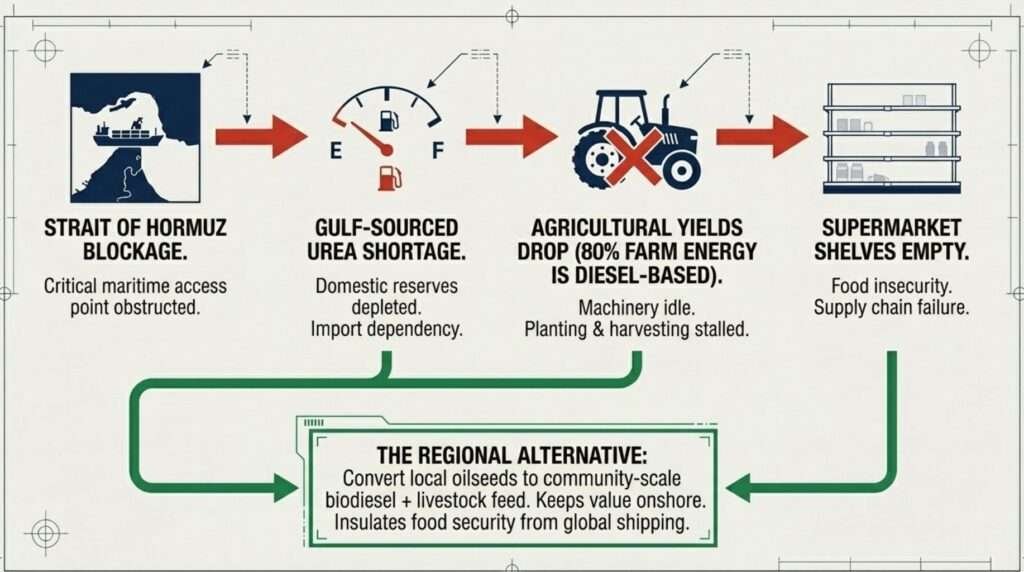

7.0 Fertiliser, Urea and the Food System Connection.

The global supply chain fragility exposed by recurring disruptions to shipping lanes does not stop at diesel. It extends directly into the agricultural systems that feed Australia and generate a significant share of its export earnings.

Fertiliser production, particularly urea and sulphur-based compounds, is concentrated in a small number of producing regions, several of which are located in or adjacent to the same geopolitically contested corridors that affect oil tanker routing.

A disruption that raises oil prices and slows tanker traffic simultaneously restricts the availability of key agricultural inputs.

The relationship is not abstract. Fertiliser prices shape planting decisions. Planting decisions determine yields.

Yields determine what arrives on supermarket shelves. The supply chain that connects a disrupted shipping lane to a gap on a grocery shelf is shorter than most urban consumers appreciate and considerably more direct than policymakers typically acknowledge.

Australia imports most of its urea from Gulf region sources. The Perdaman urea project in Western Australia represents a significant domestic production opportunity, but it will not reach full operational capacity until the latter part of this decade.

In the interim, Australia remains exposed to a specific and well-documented vulnerability: a urea supply shock can immobilise the national freight fleet and constrain agricultural production simultaneously, even if diesel supplies remain adequate.

A regional farming initiative currently under development illustrates the practical alternative. The model enables farmers to convert the oilseed crops they already grow into biodiesel at a community-scale processing facility.

Approximately 80% of farm energy use is diesel-based. By producing fuel locally from existing crops and using the residual seed meal as high-protein livestock feed, the model creates a genuinely integrated agricultural resilience system.

It reduces dependence on both imported diesel and imported feed supplements. It keeps value within regional communities rather than exporting it. This is not a theoretical proposal. It is a practical demonstration of what distributed, community-scale infrastructure can achieve when it is designed around existing assets rather than constructed around hypothetical ones.

8.0 The Resilience Gap: Where Australia Stands.

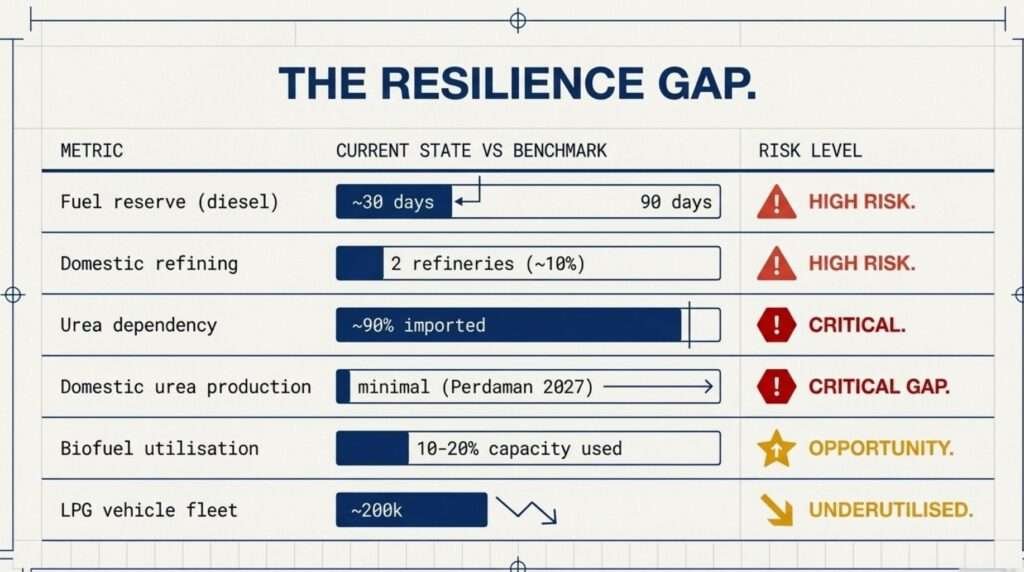

The following table places Australia’s current fuel and resilience metrics in the context of international benchmarks and the specific vulnerabilities that define the national risk profile.

Resilience Metric | Australia Current | IEA Benchmark | Risk Level |

Fuel reserve (diesel) | ~30 days | 90 days | High |

Domestic refining capacity | 2 refineries (~10% of needs) | Varies by nation | High |

Urea import dependency | ~90% imported | Domestic or diversified | Critical |

Biofuel production utilisation | 10-20% of capacity | Demand-driven | Opportunity |

Trade by sea volume | ~99% | Island nation average | Medium-High |

LPG vehicle fleet | ~200,000 (declining) | Policy-dependent | Underutilised |

Domestic urea production | Minimal (Perdaman 2027) | Strategic reserve target | Critical gap |

The pattern across these metrics is consistent. Australia’s current position reflects a system optimised for cost efficiency in stable conditions. It is not designed for resilience.

The gap between the current state and an adequate resilience position is wide, but it is not unbridgeable. Each metric in the table above represents a specific, addressable policy target.

9.0 LPG: A Strategic Asset Without a Strategy.

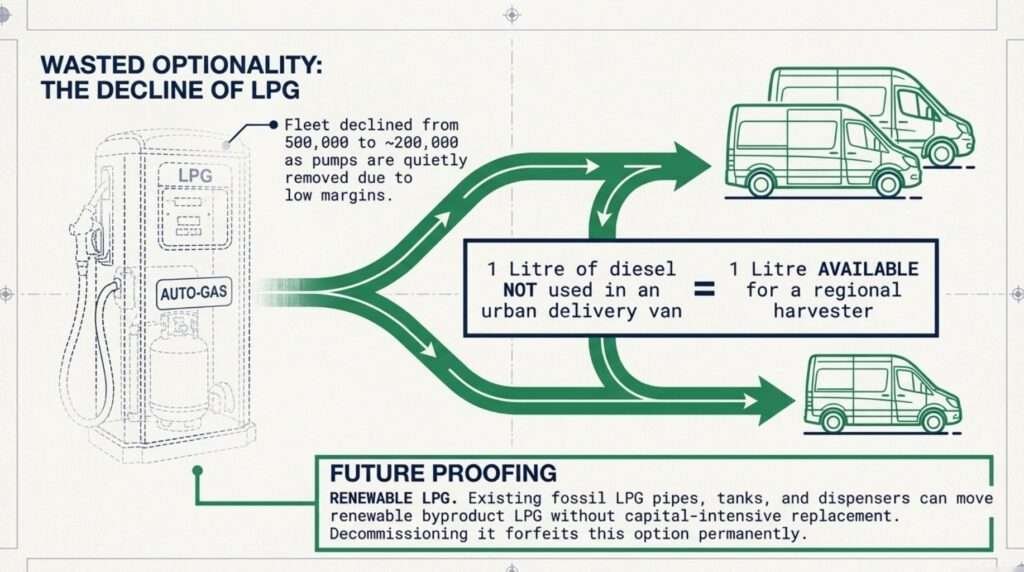

Australia once led the world in autogas adoption. Hundreds of thousands of liquefied petroleum gas vehicles moved through a dense, nationally distributed refuelling network.

The infrastructure was built, the technical knowledge was established and domestic production was sufficient to supply the transport sector while maintaining export capacity.

Today, the LPG vehicle fleet has declined from approximately five hundred thousand units in the early 2010s to around two hundred thousand.

Service station operators have been quietly removing underused LPG pumps, citing the economics of maintaining tightly regulated, low-margin infrastructure for a declining customer base.

The reasons for the decline are genuine. Petrol and diesel engines have become substantially more efficient.

Hybrid vehicles deliver meaningful fuel savings without requiring separate fuel tanks or refuelling infrastructure.

Government incentives for LPG conversion were allowed to lapse without a strategic decision about whether LPG should continue to play a role in Australia’s transport energy mix.

That absence of a strategic decision is itself a decision. And it has costs.

LPG is not a direct substitute for diesel in heavy freight and agriculture.

It suits spark-ignition engines, not the compression-ignition workhorses that keep Australia’s supply chains operating.

However, the relevant question is not whether LPG can replace diesel in semi-trailers. It is how much diesel could be freed up for high-priority uses if LPG were deliberately deployed in urban light commercial fleets, government vehicles, courier networks and taxi and rideshare services.

Every litre of diesel not consumed in an urban delivery van is a litre available for a farmer running a harvester in a remote paddock. The arithmetic is straightforward. The policy will to act on it has not materialised.

There is an additional dimension that receives almost no policy attention. Renewable LPG, a by-product of certain biodiesel and renewable diesel production processes, could progressively substitute for conventional LPG across the same infrastructure network.

The pipes, tanks and dispensing equipment that currently move fossil LPG could move renewable LPG without capital-intensive replacement.

Treating the existing LPG network as a relic to be decommissioned forfeits that optionality permanently. Treating it as a resilience asset worth maintaining and expanding preserves it.

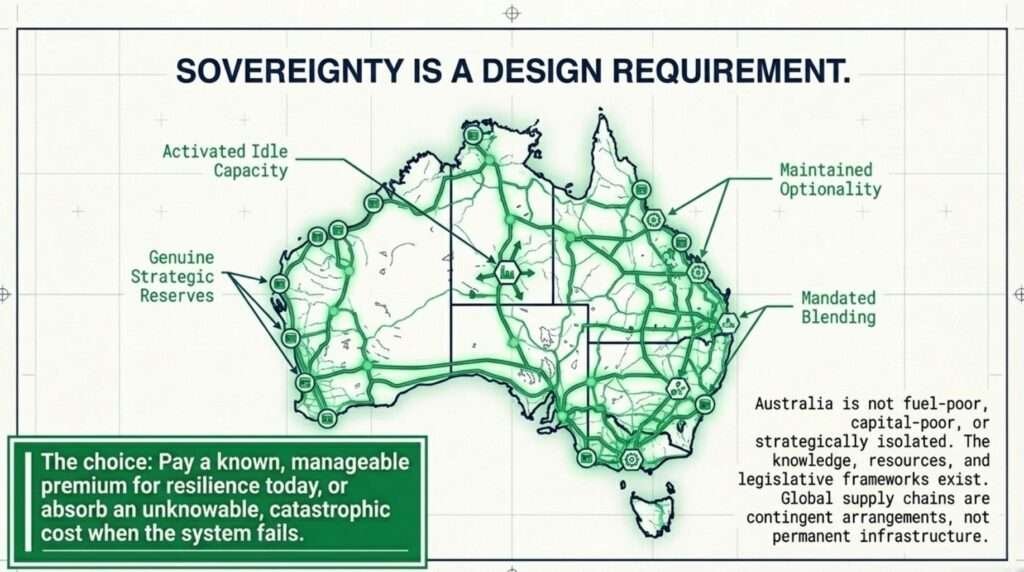

10.0 What Genuine Resilience Requires.

Resilience is not a storage metric. It is a design principle. A system built for resilience behaves differently from a system built for efficiency and the difference becomes visible precisely when conditions depart from the norm.

For Australia, a genuine resilience framework requires simultaneous action across four dimensions: onshore reserves, domestic production capacity, supply diversification and demand management.

Onshore reserves must reach a level that provides meaningful insulation from short-to-medium-term supply disruptions.

The International Energy Agency’s ninety-day benchmark exists for good reason. It represents approximately the time required to arrange alternative supply, adjust demand patterns and navigate the diplomatic and logistical processes that accompany a major supply shock.

Australia’s current reserve position provides a fraction of that buffer.

Domestic production capacity means activated, operating facilities, not idling plants and approved projects that exist on paper.

The three east-coast biodiesel facilities that currently operate at ten to 20% utilisation represent an immediately available increment of domestic fuel production. The two operating refineries at Geelong and Lytton represent a foundation that can be expanded and upgraded rather than managed toward decommissioning.

The modular refinery technologies that have matured in recent years offer a pathway to distributed, geographically dispersed refining capacity that is far less vulnerable to single-point disruption than the centralised refinery model of the twentieth century.

Supply diversification means reducing dependence on any single corridor, any single source country, or any single supply chain architecture. For fuel, that means a combination of domestic production, strategic reserves, diversified import sources and alternative fuels.

For urea and fertiliser, it means pre-purchasing from non-Gulf sources as a bridge to domestic production, establishing strategic reserves at inland hubs rather than coastal ports and using existing legislative powers to prioritise automotive-grade urea production during shortage conditions.

Demand management means having a tested, legislated framework for prioritising essential uses during supply constraints.

A formal fuel priority structure that protects agriculture, freight, emergency services and defence, while managing discretionary urban consumption, is not a rationing measure in the pejorative sense. It is a triage system for an essential resource.

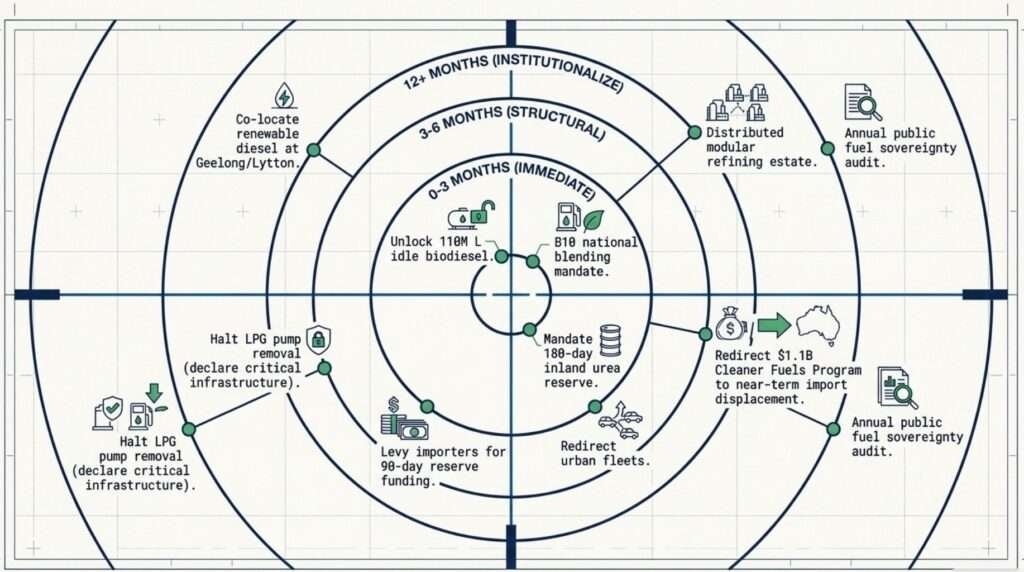

11.0 A Practical Agenda: Four Horizons of Action.

The actions required to meaningfully improve Australia’s resilience position are not experimental.

They do not depend on unproven technologies, unallocated budgets, or industries that need to be created from scratch.

They depend on activating what already exists.

11.1 Immediate Horizon (0–3 Months): Unlocking Idle Capacity.

Emergency subsidies to run the three east-coast biodiesel facilities at full capacity would unlock one hundred and ten million litres of annual domestic production using feedstocks currently exported.

A national B10 blending mandate, implemented through emergency powers under existing fuel standards legislation, would immediately displace a meaningful share of imported diesel with domestic product. Most modern diesel engines are already certified to operate on B20 blends; a B10 mandate is within existing tolerances for the overwhelming majority of the fleet.

A strategic urea reserve, mandated at one hundred and eighty days of national consumption and stored at inland hubs rather than coastal ports, would close the most acute single vulnerability in the national resilience picture.

Urea is the component that makes a full diesel tank irrelevant if it runs out.

11.2 Medium Horizon (3–6 Months): Structural Reinforcement.

Declaring the existing LPG refuelling network as critical infrastructure and halting the removal of pumps preserves optionality that cannot be rebuilt cheaply.

Conversion incentives for urban light commercial fleets, government vehicles and taxi and rideshare operators would redirect diesel from discretionary urban use to high-priority agricultural and freight applications.

Raising onshore reserve minimums to the IEA ninety-day standard, funded through a modest per-litre levy on importers distributed across the consumer base over time, transforms the reserve position without requiring sovereign capital expenditure at scale.

11.3 6–12 Month Horizon: Domestic Production Rebuild.

Fast-tracking the co-location of renewable diesel and biodiesel processing at the Geelong and Lytton refinery sites, using the feedstocks, pipelines and existing infrastructure that are already present, could displace a meaningful share of liquid fuel imports by the end of a calendar year.

The one point one billion dollar Cleaner Fuels Program represents exactly the kind of capital that should be redirected from long-horizon demonstration projects to near-term displacement of imports.

11.4 12+ Month Horizon: Institutionalising Fuel Sovereignty.

The twelve-plus month horizon is about locking in the systemic changes that prevent the next crisis from developing along the same lines as the current one: a distributed refining estate, an annual public fuel sovereignty audit with transparent reporting and the institutional habits of a nation that treats energy security as a design requirement rather than a policy aspiration.

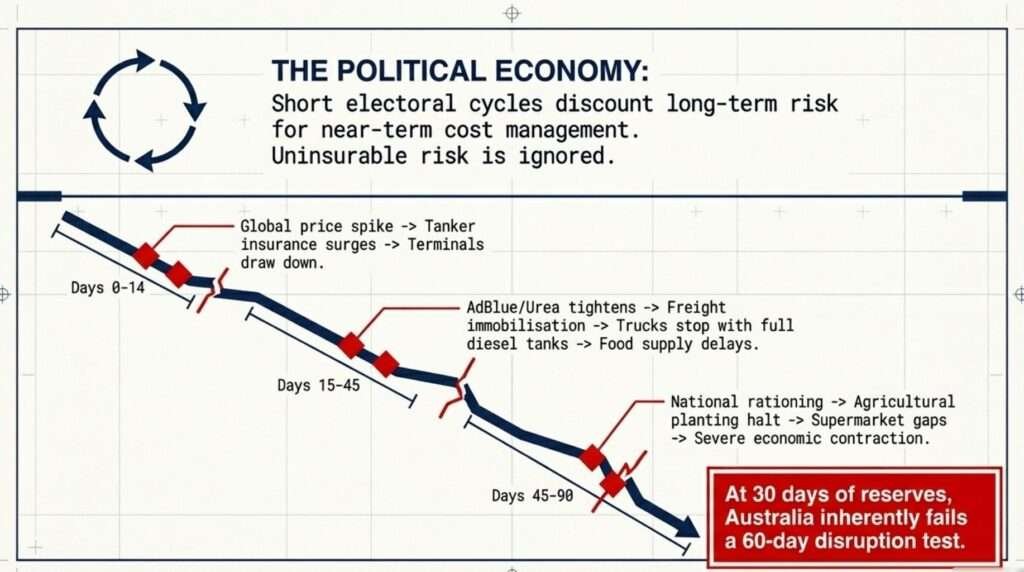

12.0 The Political Economy of Urgency.

The gap between what Australia needs to do and what it has done is not primarily a technical gap. The knowledge exists. The resources exist.

The legislative frameworks, imperfect as they are, exist.

The gap is political. Short electoral cycles create incentive structures that consistently discount long-term risk in favour of near-term cost management.

Fuel stockholding requirements were only materially strengthened in 2023, decades after the structural vulnerabilities they address were clearly visible.

Biofuel mandates in New South Wales and Queensland were introduced, poorly enforced and never scaled. LPG was allowed to peak and decline without a deliberate decision about its strategic role. The pattern repeats across each element of the resilience picture.

The cost of inaction is not evenly distributed. When fuel supply tightens, the consequences arrive first and hardest in the places that are furthest from supply hubs and most dependent on diesel: regional farming communities, remote towns, First Nations communities that depend entirely on diesel generation for electricity.

Urban consumers experience higher prices. Rural and remote communities experience supply gaps, machinery that cannot run and food production that slows or stops.

Defence capability is a separate but connected dimension.

A nation whose fuel reserves can be measured in weeks, whose urea imports pass through contested maritime corridors and whose freight network would begin to slow within days of a sustained shipping disruption is not in a position to sustain a prolonged operational response to a strategic challenge.

Fuel security and defence capability are not separate policy domains; they are the same problem viewed from different angles.

The practical trade-off is specific and worth stating plainly. Raising onshore fuel reserves to the IEA benchmark, activating idle biodiesel capacity, mandating blending requirements and establishing a strategic urea reserve will add costs. Those costs will be visible and immediate.

They will appear in fuel prices, in budget line items and in the margins of industries that currently benefit from the efficiency of the just-in-time system.

The cost of the alternative, a supply disruption of sufficient duration to cause freight network slowdown, agricultural production loss and cascading economic failure, is orders of magnitude larger and essentially uninsurable.

The choice is between paying a known, manageable premium for resilience or absorbing an unknowable and potentially catastrophic cost when the system fails. That is not a difficult calculation. It has simply not been the one that drives policy.

12.1 Scenario Analysis: A 60 Day Supply Disruption.

A structural vulnerability becomes tangible when examined through a plausible scenario. So let’s now consider a sixty‑day disruption to tanker traffic through the Strait of Hormuz from geopolitical escalation.

Weeks 1–2:

· Global oil prices spike.

· Tanker insurance surges.

· Australian terminals draw down inventories.

Weeks 3–6:

· Reduced tanker arrivals tighten wholesale markets.

· Regional supply chains (farming, remote towns) face first delays.

· Importers prioritise metro hubs.

Urea shock hits faster:

· AdBlue inventories tighten within 3–4 weeks.

· Freight fleets reduce operations, trucks stop even with full diesel tanks.

· Agricultural planting/harvesting slows.

Cascading effects:

· Freight capacity drops 20–30%, delaying food/medical supplies.

· Regional fuel queues emerge.

· Supermarket gaps from disrupted planting decisions.

· Defence/emergency services ration diesel.

Impact Timeline | Fuel Effect | Urea Effect | Cascades |

0–14 days | Price spike | Stockpile drawdown | None immediate |

15–45 days | Regional shortages | Freight immobilisation | Food supply delays |

45–90 days | National rationing | Agricultural halt | Economic contraction |

This isn’t a doomsday scenario, not at all; it’s a system test revealing design flaws. Our current position is 30 days of reserves, so 90% import reliance fails this test in my opinion.

13.0 Conclusion.

Australia is not fuel-poor, capital-poor, or strategically isolated. It is an island nation with extraordinary natural resources, a highly educated population, functional institutions and a geography that, properly understood, is a strategic advantage rather than a liability.

What it has not yet built is a national system designed around the reality that global supply chains are contingent arrangements, not permanent infrastructure.

The recurring instability in the Middle East, the periodic disruptions to global shipping lanes, the structural fragility of fertiliser and urea supply chains and the documented vulnerability of maritime chokepoints are not exceptional events.

They are recurring features of the environment in which Australia operates.

Building resilience to those features requires treating fuel sovereignty as a design requirement: mandating blending, activating idle production capacity, establishing genuine strategic reserves, maintaining infrastructure that provides optionality rather than decommissioning it and creating the legislative and operational frameworks that allow essential functions to continue when the global system tightens.

None of the actions required are radical. They do not require invented technologies, speculative funding, or industries that do not yet exist.

They require using the assets, the laws and the capital that Australia already has, directed by a political will that matches the scale of the risk.

The cost of building that resilience is measurable and manageable. The cost of choosing not to build it will be neither.

14.0 Bibliography.

1. International Energy Agency (2025). Oil Security Emergency Response. IEA Paris

https://www.iea.org/reports/oil-security-emergency-response

2. Department of Climate Change, Energy, Environment & Water (2025). Liquid Fuel Security Review. DCCEEW Canberra

https://www.energy.gov.au/publications/liquid-fuel-security-review-2025

3. Australian Competition & Consumer Commission (2025). Quarterly Petroleum Monitoring Report Q4. ACCC Sydney

https://www.accc.gov.au/publications/petroleum-monitoring-report-q4-2025

4. Geoscience Australia (2025). Australian Energy Resources Assessment. GA Canberra

https://www.ga.gov.au/scientific-topics/energy/resources/australian-energy-resources-assessment

5. Australian Bureau of Agricultural & Resource Economics (2025). Agricultural Commodities March 2025. ABARES Canberra

https://www.agriculture.gov.au/abares/research-topics/agricultural-outlook/agricultural-commodities

6. Fertiliser Australia (2025). Urea Market Report. Fertiliser Australia Melbourne

https://www.fertiliser.org.au/urea-market-report-2025

7. Australian Institute of Petroleum (2025). Downstream Petroleum Data. AIP Melbourne

https://www.aip.com.au/resources/downstream-petroleum-data-2025

8. Australian Energy Market Operator (2025). Gas Statement of Opportunities. AEMO Melbourne

https://aemo.com.au/energy-systems/gas/gas-statement-of-opportunities-gsoo

9. Department of Industry, Science & Resources (2025). Resources & Energy Quarterly Dec 2025. DISR Canberra

https://www.industry.gov.au/data-and-publications/resources-and-energy-quarterly-december-2025

10. Australian National Audit Office (2024). Fuel Security Stockholding Arrangements. ANAO Canberra

https://www.anao.gov.au/work/performance-audit/fuel-security-stockholding-arrangements

11. Productivity Commission (2025). Supply Chain Resilience Inquiry Report. PC Canberra

https://www.pc.gov.au/inquiries/completed/supply-chain-resilience/report

12. United States Energy Information Administration (2025). World Oil Transit Chokepoints. EIA Washington

https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints

13. Department of Defence (2023). Defence Strategic Review. DoD Canberra

https://www.defence.gov.au/about/strategic-planning/defence-strategic-review

14. Grattan Institute (2025). Securing Australia’s Energy Future. Grattan Melbourne

https://grattan.edu.au/report/securing-australias-energy-future-2025

15. CSIRO (2024). Bioenergy Roadmap for Australia. CSIRO Newcastle

https://www.csiro.au/en/research/technology-space/energy/bioenergy-roadmap

16. NEMA (2025). National Disaster Risk Reduction Framework. NEMA Canberra

https://www.nema.gov.au/about-us/governance-and-reporting/strategies-and-frameworks

17. Australian Petroleum Statistics (2025). ELGAS Report Sep 2025

https://www.elgas.com.au/elgas-knowledge-hub/business-lpg/australian-petroleum-statistics-2025

18. Crude Oil Peak (2025). Australian Fuel Import Vulnerability Sep 2025

https://crudeoilpeak.info/?p=49345

19. International Maritime Organization (2025). Global Shipping Statistics. IMO London

https://www.imo.org/en/OurWork/Statistics/Pages/Default.aspx

20. ASPI (2025). National Resilience in Contested Environment. ASPI Canberra

https://www.aspistrategist.org.au/national-resilience-contested-environment-2025

[…] Should Australia Rebuild Its National Resilience? […]